Table of Contents

Summarize and analyze this article with

Chat GPT

Perplexity

Grok

Google AI

Claude

Why bank M&A integration is a technology problem before it's an integration problem

The market map: four provider types behind M&A tech integration

| Provider type | What they sell | Strong at | Weak at |

|---|---|---|---|

| M&A deal advisors / investment banks | Diligence, valuation, deal structuring | Pre-close diligence; closing | Post-close technology execution |

| Big 4 / strategy consultancies | Target operating models, integration roadmaps | Diagnosis; board narratives | Hand off before delivery; little working software |

| Software / platform vendors | Core conversion, migration, integration platforms | Mature product capabilities | Assume governed data exists |

| Implementation partners | Source-to-target mapping, MDM, lineage, reporting and model continuity, examiner-ready evidence | Building the foundation; making the integration actually work end-to-end | Not a substitute for deal advisory or the platform license |

The expensive mistake is hiring a deal advisor and a strategy firm and assuming the gap between them closes itself between announcement and Day 1. It does not that gap is the governed data foundation, the source-to-target mapping, the reporting continuity plan, and the examiner-ready evidence trail. It is where most integrations actually break.

Build vs. buy vs. partner per integration capability

| Capability | Recommended | Why |

|---|---|---|

| Pre-close technology due diligence | Partner | Engagement-specific; output is a risk register, not a product |

| Core conversion / consolidation engine | Buy | Vendor product market is mature |

| Source-to-target mapping & migration runbooks | Build / partner | Bank-specific; cannot be licensed |

| MDM, lineage, quality, golden records | Build / partner | Decides whether reporting and models survive cutover |

| Reporting continuity & reconciliation | Build / partner | Where examiner risk concentrates |

| BSA/AML & fraud-model continuity | Build / partner | Inherited models need re-baselining |

| Model & AI inventory (combined entity) | Build / partner | Required for SR 26-2 readiness post-close |

The rule of thumb for M&A tech integration

The deal advisor closes the deal. The strategy firm designs the operating model. The platform vendor sells the engine. The implementation partner builds the data foundation and runs the integration to a defensible end state without breaking a regulatory report, a BSA/AML alert, or a customer’s account. Most banks underinvest in that fourth role and pay for it after close.

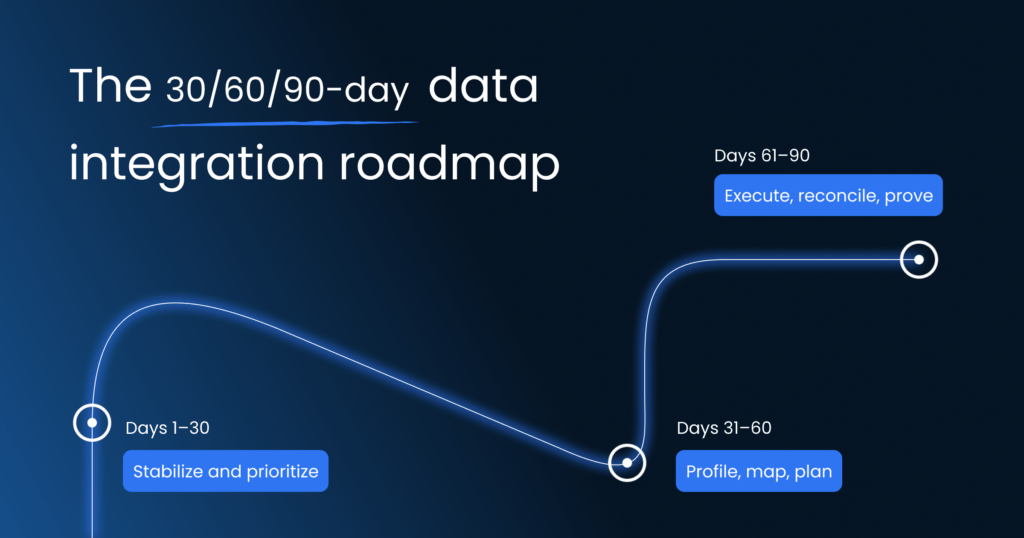

The 30/60/90-day data integration roadmap

The cadence below is what protects Day 1 and the first quarter. It is the same one PiTech uses on bank M&A engagements; the deliverables matter more than the timeline labels.

Days 1–30 — Stabilize and prioritize

- Stand up the Day 1 data risk register: critical customer/account/transaction/risk/AML/fraud/reporting domains, named owners, fallback procedures.

- Lock customer and account data continuity, BSA/AML monitoring continuity, regulatory reporting continuity, vendor-system continuity, and access controls.

- Inventory all models and AI systems inherited from both banks the combined model inventory is required for SR 26-2 readiness, regardless of integration progress.

Days 31–60 — Profile, map, plan

- Complete source-system profiling and source-to-target mapping for the highest-risk data domains first (customer, account, transaction, then loan/credit/risk).

- Capture lineage, resolve master data, profile quality and quantify remediation work.

- Plan migration waves and test sequencing; recalculate critical regulatory disclosures in parallel.

Days 61–90 — Execute, reconcile, prove

- Run controlled migration waves with reconciliation before and after each wave.

- Validate model and report continuity; document the control end-to-end so it is examiner-ready.

- Stand up post-close monitoring across the combined data estate.

The 10-criterion vendor evaluation scorecard

| # | Criterion | What ‘good’ looks like |

|---|---|---|

| 1 | Day 1 data risk discipline | Has produced a defensible Day 1 register at peer banks |

| 2 | Source-to-target mapping depth | Can show a redacted mapping artifact from a prior engagement |

| 3 | Reporting continuity track record | Has integrated a bank without breaking a regulatory report |

| 4 | Model & AI continuity | Re-baselines BSA/AML, fraud, credit, and vendor models through cutover |

| 5 | Examiner-ready evidence | Audit trail produced as a by-product |

| 6 | Banking M&A track record at your asset size | Named engagements; references with closed examiner findings |

| 7 | Pre-close + post-close coverage | Many firms do one well; verify both |

| 8 | Senior staffing | Named architect and SME for the full engagement |

| 9 | Build-vs-buy honesty | Will tell you when to buy a conversion engine rather than sell you services |

| 10 | 3-year TCO transparency | License + integration + run + actual overrun history |

RFP questions that separate integrators from advisors

- Show a banking M&A engagement where you produced the Day 1 data risk register and the bank actually used it through close.

- Show a redacted source-to-target mapping artifact from a prior bank integration.

- Describe how you protected regulatory reporting continuity through cutover in your last bank M&A engagement.

- How do you re-baseline BSA/AML and fraud models for the combined entity?

- What is your 30/60/90-day data integration roadmap, and what acceptance criteria gate each phase?

- Did the bank clear examiner findings as a direct result of your engagement? Provide a peer reference under NDA.

- Named senior staffing for the full engagement in the SOW, not a brochure?

- Three-year TCO with run-rate, and actual overrun percentages on the last three banking M&A engagements?

TCO buckets buyers underestimate

- License / subscription conversion engine, integration tooling, cloud.

- Integration & data foundation mapping, MDM, lineage, golden records, quality remediation, reporting rebuild largest bucket, the one vendors exclude.

- Run & evidence monitoring, validation, examiner-evidence upkeep through and beyond cutover.

- Cost of inaction Day 1 disruption, customer impact, reporting breaks, model degradation, deal value erosion.

ROI: where the value actually comes from

Bank M&A technology integration succeeds when the combined institution can produce, on demand, the lineage and evidence behind every consolidated control. PiTech compressed a Fortune 500 banking client’s SAS-to-IBM InfoSphere migration from 18 months to under 11 months with 100% on-time milestone delivery and zero cost overruns; 68% of data conflicts auto-resolved through entity-resolution discipline. The integration analog of that work same governance, same source-to-target mapping, same reconciliation cadence is what protects deal value through cutover.

How PiTech fits the M&A integration buying decision

PiTech is a practical implementation partner for regulated U.S. banks ($1B–$50B in assets). On M&A tech integration the work runs pre-close diligence and post-close execution as one controlled program: Day 1 data risk register; source-to-target mapping across customer, account, transaction, loan, risk, BSA/AML, finance, and reporting domains; MDM and golden records; model and report continuity; reconciliation before and after each wave. Senior practitioners deliver under CMMI Level 3 and ISO 27001/9001/42001 discipline. Explore the Mergers & Acquisition practice, the Banking Hub, review the comparison piece Top Bank M&A Technology Integration Partners 2026, or book a 30-minute banking discovery call.

Frequently Asked Questions (FAQs)

What does bank M&A technology integration include?

How do you choose a bank M&A integration partner?

Score candidates on Day-1 data risk discipline, source-to-target mapping depth, reporting-continuity track record, model and AI continuity discipline, examiner-ready evidence, banking M&A track record at your asset size, both pre-close and post-close coverage, named senior staffing for the full engagement, build-vs-buy honesty, and transparent three-year total cost of ownership including overrun history. Weight reporting continuity and examiner-evidence criteria heavily.

What is a Day-1 data risk register?

A Day-1 data risk register is the authoritative pre-close artifact identifying the data domains, reports, models, customer operations, access controls, vendors, and regulatory obligations that cannot break at close with named owners, reconciliation checkpoints, fallback procedures, and decision rights for urgent exceptions. It is the single most useful artifact a Day-1 program produces, and its absence is the most reliable predictor of an integration that breaks something material around close + 30 days.

Which data domains carry the highest risk during bank integration?

Customer master data, account and product data, transaction history, loan and credit data, BSA/AML and sanctions data, fraud signals, risk and finance data, regulatory reporting feeds, model inputs (including inherited and vendor models), and third-party system dependencies. Privacy and access-control risk rise when consent rules, retention policies, identifiers, and access roles differ between the two banks. Safe integration starts with source profiling and golden-record discipline before any technical migration begins.

How do you protect regulatory reporting continuity during a core conversion?

Every regulatory report has to keep producing through cutover with lineage, definitions, controls, and reconciliation evidence intact. Start by inventorying every report impacted by source-system changes, mapping upstream fields across both banks, recalculating disclosures in parallel for at least two cycles, retaining audit evidence through the transition, and locking reconciliation checkpoints before and after each migration wave. CECL, capital, stress-testing, BSA/AML, and Call Reports are most exposed.

What about BSA/AML model migration after a merger?

How does SR 26-2 affect a post-merger model inventory?

After a bank merger the model inventory must be re-baselined for the combined institution because it may inherit duplicate, overlapping, vendor-supplied, or poorly documented models. SR 26-2 (April 2026) re-baselined model risk expectations: the inventory should include traditional models, ML models, GenAI use cases, agentic workflows, vendor models, owner, purpose, data inputs, risk tier, validation status, monitoring metrics, and retirement/change controls. The GenAI/agentic carve-out is the bank’s own to govern.

What should be in a bank merger data migration RFP?

Scope for data discovery, source-system profiling, source-to-target mapping, MDM, lineage, quality remediation, reconciliation before and after each wave, cutover planning, reporting continuity, BSA/AML and fraud-model continuity, security and privacy through cutover, third-party coordination, post-close monitoring, and named senior staffing across all of it. Ask for actual overrun percentages and references with closed examiner findings, not narrative case studies.

How long does bank M&A technology integration take?

A defensible Day 1 plus a first-quarter integration win is achievable in roughly 90 days with the right partner and a focused scope. Full data-estate integration is typically 12–24 months for mid-market banks, driven by asset size, the number of source systems, the condition of the data layer, and the complexity of regulatory reporting. Cutover timing should be set by reconciliation readiness, not by calendar; rushed cutovers concentrate risk.

What does failed bank M&A integration look like?

Weak source profiling produces surprises around close + 30 days. Unclear ownership leaves data without stewards. Poor product/account mapping breaks reporting. Insufficient testing concentrates defects at cutover. Privacy gaps surface under regulator scrutiny. Lack of post-conversion reconciliation hides errors that compound. The real risk is not project delay; it is operational disruption, regulatory exposure, customer impact, and loss of trust in the combined bank’s data which erodes deal value directly.