Table of Contents

Summarize and analyze this article with

Chat GPT

Perplexity

Grok

Google AI

Claude

Why reporting continuity is the test examiners actually run

The reports most exposed by integration

| Report | Why exposed | Watch closely |

|---|---|---|

| Call Report (FFIEC 031/041/051) | Touches almost every data domain | Field-level mapping across both banks |

| CECL | Depends on loan, credit, and risk data | Segmentation; loss methodology continuity |

| Capital (FFIEC 101) | Depends on risk-weighted assets | RWA recalculation across combined exposures |

| Liquidity (5300, LCR/NSFR where applicable) | Depends on funding and cash-flow data | Combined funding profile reconciliation |

| Stress testing | Multi-domain inputs | Scenario re-validation on combined data |

| BSA/AML & SAR filings | Depends on transaction monitoring | Alert continuity through cutover |

| HMDA & fair-lending | Application-level loan data | Cross-bank field harmonization |

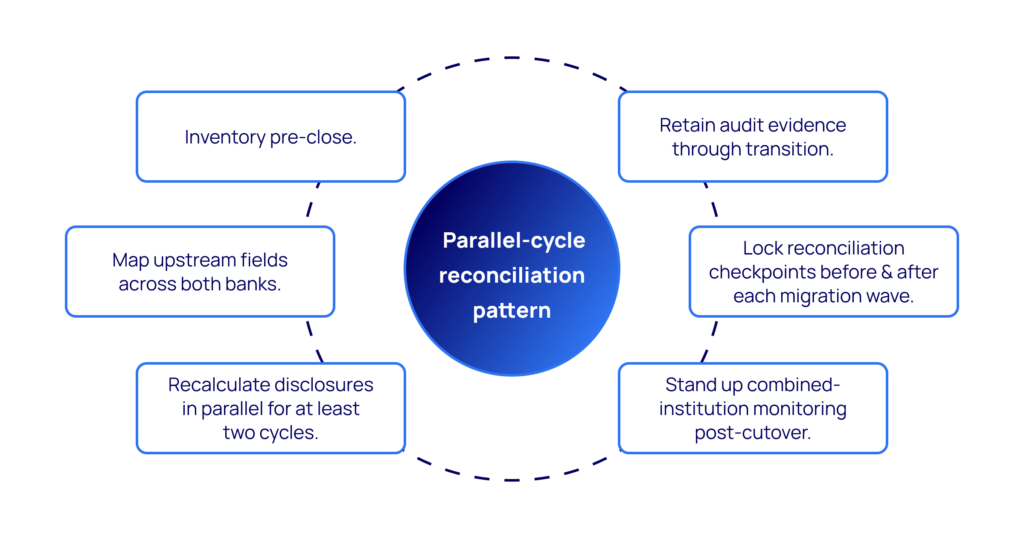

The parallel-cycle reconciliation pattern

- Inventory pre-close. Identify every regulatory report impacted by source-system changes, with named owner, frequency, dependencies, and audit-evidence requirements.

- Map upstream fields across both banks. Source-to-target at field level, not domain level.

- Recalculate disclosures in parallel for at least two cycles. Both pre-cutover and post-cutover; document variance and root cause.

- Retain audit evidence through transition. Lineage, definitions, controls, reconciliation results kept queryable, not boxed up.

- Lock reconciliation checkpoints before and after each migration wave. Acceptance criteria gate the next wave.

- Stand up combined-institution monitoring post-cutover. Drift detection; outlier review; refreshed reconciliation cadence.

Acceptance criteria, not narrative

SOW asks that protect reporting continuity contractually

- Day-1 reporting register in deliverable list, owned by named integration leads.

- Field-level source-to-target mapping for every impacted report, redacted artifact reviewable pre-signature.

- Minimum two parallel-cycle reconciliations with tolerance bands and pass/fail criteria specified.

- Examiner-evidence packaging produced as a by-product of the reporting process, not at examination time.

- Named senior reporting SME in working sessions for the full engagement.

- Acceptance gating between migration waves tied to reconciliation outcomes.

A partner test specific to reporting continuity

- Show a banking merger engagement where you migrated source systems without breaking a regulatory report.

- Describe the reconciliation cadence tolerances, frequencies, sign-offs used in your last bank M&A engagement.

- How did you handle CECL segmentation continuity through a merger? Walk through a specific example.

- What evidence package did you hand to examiners post-conversion?

- Did the bank clear examiner findings as a direct result of your engagement? Reference under NDA?

Anti-patterns

- Reporting continuity as a post-cutover cleanup. Examiners evaluate the day, not the cleanup.

- Domain-level mapping passed off as field-level. Domain-level mapping looks tidy and produces field-level reporting errors.

- Single-cycle reconciliation. One pre-cutover and one post-cutover cycle is the minimum; one cycle hides drift.

- Narrative reconciliation in lieu of acceptance criteria. Variances need tolerance bands and pass/fail outcomes, not paragraphs.

- Vendor sign-off without senior reporting SME presence. Reconciliation sign-off is not a procedural box-check.

How PiTech protects reporting continuity

PiTech treats reporting continuity as a Day-1 commitment, not a post-cutover cleanup. The work spans Day-1 reporting register, field-level source-to-target mapping across both banks, parallel-cycle reconciliation with specified tolerance bands, audit-evidence packaging produced as a by-product, and acceptance gating between migration waves. Named senior reporting SMEs deliver under CMMI Level 3 and ISO 27001/9001/42001 discipline.

Frequently Asked Questions (FAQs)

How do banks protect regulatory reporting through a merger?

Which regulatory reports carry the highest integration risk?

Call Report (FFIEC 031/041/051), CECL, capital reporting (FFIEC 101), liquidity reporting (5300 and LCR/NSFR where applicable), stress testing, BSA/AML and SAR filings, and HMDA/fair-lending. These reports depend on the most data domains and therefore concentrate cross-bank field harmonization risk. Each should be on the Day-1 reporting register with a named owner.

How many parallel reporting cycles should run during conversion?

At least two one pre-cutover and one post-cutover for each impacted reporting cadence. One cycle hides drift and prevents root-cause investigation. Two cycles with documented variance and tolerance bands establish whether the new platform is producing defensible numbers consistently. For high-risk reports (CECL, capital, stress testing) more cycles may be required by internal policy or external auditor expectations.

What does field-level source-to-target mapping mean?

Field-level mapping documents how every individual data field in a regulatory disclosure is sourced, transformed, and aggregated from both banks’ source systems into the target platform’s reporting layer. Domain-level mapping (e.g., ‘customer data goes here’) looks tidy in a deck but produces field-level reporting errors at cutover. Examiners ask field-level questions; the mapping artifact must support field-level answers.

How are CECL and credit reporting protected through a merger?

What about BSA/AML reporting continuity?

Alert generation, sanctions screening, and SAR filings must continue uninterrupted through cutover. Transaction monitoring models, thresholds, customer risk scoring, and screening lists need to be re-baselined against the combined data estate. Historical case data should be made queryable for analyst follow-up. The combined entity’s BSA/AML continuity is part of the reporting continuity story, not separate from it.

What evidence should be packaged for examiners?

Lineage from source field through transformation to disclosed number, definitions for every reportable field, control documentation, reconciliation results with tolerance bands and pass/fail outcomes, named owners, and the audit trail of any defects encountered and remediated. Package this as a by-product of the reporting process, queryable on demand, not assembled at examination time. The test is: can an examiner ask ‘show me how this number was produced’ and get an answer in minutes?

How do we handle reporting differences between the two banks?

Many mergers inherit minor differences in reporting methodology, segmentation, or vendor models. Inventory the differences, decide which approach the combined institution will adopt, document the rationale for board and auditor visibility, and recalculate at least two prior-period disclosures under the new approach to expose any reporting impact. Methodology changes hidden inside integration noise become examiner findings later.

Should the reporting team or the integration team own reporting continuity?

Both co-ownership with explicit decision rights. The reporting team owns acceptance criteria, tolerance bands, and sign-off authority for each reconciliation cycle. The integration team owns field-level mapping, source-system profiling, migration wave execution, and remediation of identified defects. Single-team ownership concentrates risk on the side that did not get involved early enough.

What metrics show reporting continuity went well?

Zero unplanned regulatory reporting breaks. Parallel-cycle reconciliation pass rates inside specified tolerance bands. Field-level mapping coverage at 100% for every impacted report. Examiner evidence retrievable on demand in minutes from the system. Findings closed (or none opened) within the integration window. ‘Reports filed on time’ is necessary but not sufficient the test is whether the numbers are defensible at field level under examination.