Table of Contents

Summarize and analyze this article with

Chat GPT

Perplexity

Grok

Google AI

Claude

What CFPB Circular 2022-03 actually requires

The three strategy patterns

CFPB Circular 2022-03 confirms that ECOA’s adverse-action notification requirements apply to credit decisions made using complex algorithms including machine-learning and AI models. A bank that denies, terminates, or unfavorably changes the terms of an existing credit account must provide a statement of specific principal reasons for the action. Generic reasons, model-output-only reasons, or ‘the model decided’ are not acceptable. The bank is responsible regardless of whether the model is in-house, vendor-supplied, or built on a hosted ML platform.

The Circular does not prescribe a particular explainability method; it requires accuracy and specificity in the principal reasons. Banks that use complex models in credit decisioning must therefore select explainability methods, validate their accuracy, integrate them into the adverse-action workflow, and document the decision trail in a way that examiners can review.

Required artifacts for a defensible program

- Explainability method per model class. Document which method (SHAP, LIME, surrogate models, native logistic explainers, etc.) applies to each model class and why it is appropriate.

- Adverse-action workflow integration. The explainability output flows automatically into the adverse-action notice generation, with mapping from input features to ECOA-compliant reason codes.

- Reason-code accuracy validation. Periodic validation that the explainability method produces accurate, specific reasons; documented and reviewed by MRM.

- Decision trail logging. For every credit decision, log the model version, input features, output, principal reasons, and adverse-action notice sent queryable for examiner review.

- Vendor model treatment. If the credit model is vendor-supplied, the bank requires the vendor to provide explainability outputs sufficient for ECOA-compliant reason codes, and validates them not the vendor’s claims about them.

- Fair-lending integration. Explainability outputs feed into disparate-impact testing and fair-lending monitoring.

Vendor RFP questions specific to credit AI partners

- Which explainability method does your model use, and why is it appropriate for our credit decisioning?

- Show an adverse-action notice generated end-to-end from a denial through your system with the principal reasons, the workflow, and the audit trail.

- How do you validate the accuracy of your explainability outputs?

- What is the integration model for our adverse-action notice generation and our fair-lending monitoring?

- How do you handle credit decisions where the model’s confidence is low or the explanation is ambiguous?

- Which peer banks have used your model in production and cleared examinations on it?

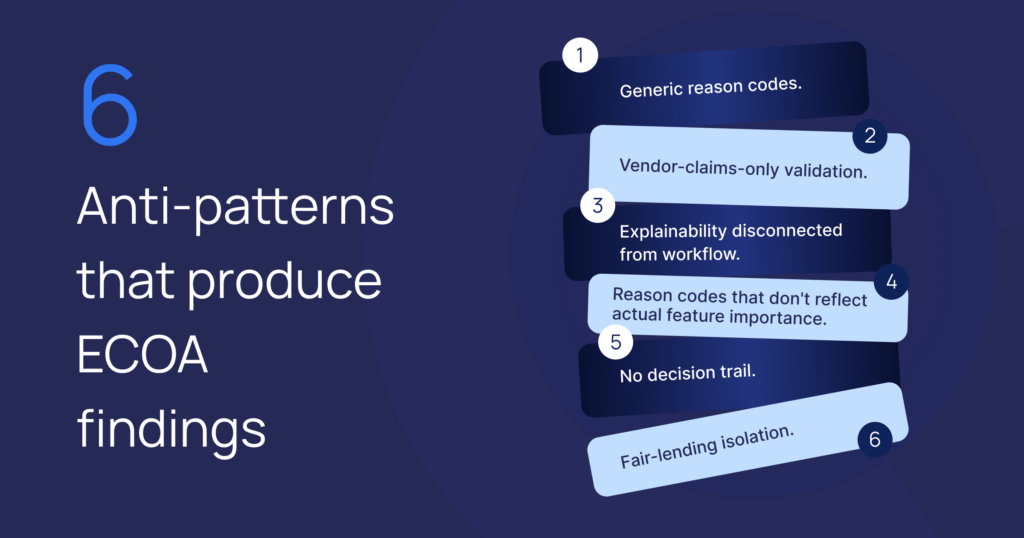

Six anti-patterns that produce ECOA findings

- Generic reason codes. ‘Insufficient credit profile’ for every denial is not specific. The Circular requires accurate, specific principal reasons.

- Vendor-claims-only validation. Treating the vendor’s claim that the model is ‘explainable’ as the bank’s validation.

- Explainability disconnected from workflow. An explainability dashboard that no one consults during adverse-action notice generation.

- Reason codes that don’t reflect actual feature importance. Mapped reasons that bear no relationship to which features actually drove the denial.

- No decision trail. Adverse-action notice sent without a queryable log of model inputs, output, and principal reasons.

- Fair-lending isolation. Credit AI explainability that does not feed disparate-impact testing or fair-lending monitoring.

Operating model integration

Credit AI explainability lives at the intersection of three operating models: model risk (the explainability method is part of the validation evidence), adverse-action workflow (the reasons flow into notices), and fair-lending (the reasons feed disparate-impact and monitoring). A program that treats explainability as a model-risk-only concern misses the workflow integration; a program that treats it as a workflow-only concern misses the validation discipline; a program that treats it as a fair-lending-only concern misses the model-risk anchoring. All three integrations are required.

How PiTech approaches credit AI explainability

Frequently Asked Questions (FAQs)

What does CFPB Circular 2022-03 require for credit AI?

What is credit AI explainability in practice?

Credit AI explainability is the operational connection between a credit model’s output, the input features that drove the decision, the policy framework, and the ECOA-compliant principal-reasons statement sent to the applicant. It includes the explainability method (SHAP, LIME, surrogate models, native explainers), the validation of the method’s accuracy, the workflow integration into adverse-action notices, the decision trail logging, and the fair-lending monitoring feedback.

Which explainability method should a bank use?

The right method depends on the model class. For tree-based ensembles, SHAP is common and well-validated. For linear or logistic models, native coefficient explainers may be sufficient. For deep learning or opaque vendor models, surrogate models or specialized explainability tooling may be required. Document the method per model class, validate its accuracy, and review periodically. The Circular does not prescribe a method; it requires accuracy and specificity in the principal reasons.

What does a defensible credit AI program need?

Six artifacts: an explainability method documented per model class with rationale, adverse-action workflow integration with mapping from input features to ECOA-compliant reason codes, periodic validation of reason-code accuracy reviewed by MRM, decision-trail logging queryable for examiner review, vendor-model treatment (explainability outputs validated by the bank, not by vendor claim), and fair-lending integration where explainability feeds disparate-impact testing.

Is the bank responsible if the credit model is vendor-supplied?

Yes. The bank is responsible for ECOA compliance regardless of model ownership. A vendor-supplied credit model requires the bank to receive explainability outputs sufficient for ECOA-compliant principal reasons, validate the accuracy of those outputs (not the vendor’s claims about them), and document the validation. ‘The vendor told us the model is explainable’ is not a defense the CFPB accepts.

Can a complex model be too opaque to use?

A model that cannot produce accurate, specific principal reasons should not be used in U.S. credit decisioning, because the adverse-action notice cannot be ECOA-compliant. The Circular does not require the model itself to be transparent; it requires the bank to produce accurate, specific principal reasons. If no available explainability method can produce them for the model class, the model is not deployable in credit. Choose a different model or a different explainability approach.

How does fair-lending integrate with credit AI explainability?

Explainability outputs feed disparate-impact testing and ongoing fair-lending monitoring. If the explainability method identifies that a feature drove denials more in one protected class than another, the fair-lending team has the signal to investigate and the model-risk team has the signal to validate or retrain. A credit AI program without this integration produces principal reasons that do not feed fair-lending discipline, which surfaces as a finding later.

What's the most common credit AI compliance failure?

Generic reason codes ‘insufficient credit profile’ for every denial are the most common ECOA finding under Circular 2022-03. The Circular specifically calls out generic reasons as inadequate. The fix is mapping explainability outputs to specific, accurate principal reasons per denial, validating the mapping, and logging the decision trail for examiner review.

How long does credit AI explainability build-out take?

For a focused scope one to three credit models in production with adverse-action workflow integration, validation, and fair-lending feedback the build-out typically runs 60–90 days. Vendor-model engagements may take longer due to vendor coordination on explainability outputs. Banks with credit AI already in production should prioritize this work; banks planning credit AI deployment can build the explainability framework first and apply it to models as they enter intake.

How is examiner-ready evidence packaged?

For each credit AI model: the explainability method and validation evidence, sample adverse-action notices end-to-end (input features → output → principal reasons → notice), decision-trail logs queryable on demand, fair-lending integration evidence, vendor documentation where applicable, and ongoing validation cadence records. The package is maintained continuously, not assembled at examination time.