Table of Contents

Summarize and analyze this article with

Chat GPT

Perplexity

Grok

Google AI

Claude

Why 'strategy' matters more than 'platform' in legacy modernization

The three strategy patterns

1. Rip-and-replace

2. Coexistence (parallel run)

3. Hollow-out (strangler pattern)

Keep the legacy core as system-of-record for ledger continuity and move capabilities customer experience, analytics, AI/ML, new products to a modern data and services layer around it. Lowest disruption to ledger and reporting, requires the strongest data and integration discipline. Often the right pattern when the legacy core is stable but constraining innovation.

A decision matrix for choosing the pattern

| Factor | Rip-and-replace | Coexistence | Hollow-out |

|---|---|---|---|

| Asset size sweet spot | <$5B | $5B–$50B | Any |

| Disruption risk | High | Medium | Low |

| Reporting continuity | Hardest to protect | Best protected | Best protected |

| Time to target | Fastest | Medium | Slowest |

| Data foundation required | Very high | High | Very high |

| Vendor concentration risk | Highest | Medium | Low |

What examiners ask, regardless of pattern

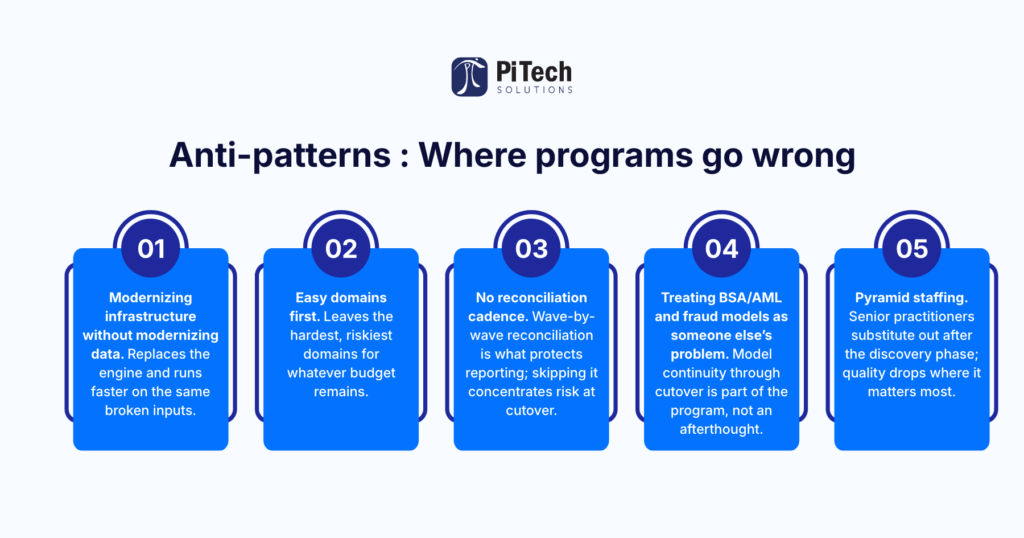

- Modernizing infrastructure without modernizing data. Replaces the engine and runs faster on the same broken inputs.

- Easy domains first. Leaves the hardest, riskiest domains for whatever budget remains.

- No reconciliation cadence. Wave-by-wave reconciliation is what protects reporting; skipping it concentrates risk at cutover.

- Treating BSA/AML and fraud models as someone else’s problem. Model continuity through cutover is part of the program, not an afterthought.

- Pyramid staffing. Senior practitioners substitute out after the discovery phase; quality drops where it matters most.

Anti-patterns: where programs go wrong

- Modernizing infrastructure without modernizing data. Replaces the engine and runs faster on the same broken inputs.

- Easy domains first. Leaves the hardest, riskiest domains for whatever budget remains.

- No reconciliation cadence. Wave-by-wave reconciliation is what protects reporting; skipping it concentrates risk at cutover.

- Treating BSA/AML and fraud models as someone else’s problem. Model continuity through cutover is part of the program, not an afterthought.

- Pyramid staffing. Senior practitioners substitute out after the discovery phase; quality drops where it matters most.

A vendor-screening lens specific to legacy modernization

- Show an engagement where you ran legacy and modern cores in parallel and reconciled across every wave.

- What does your source-to-target mapping artifact look like? Show a redacted one.

- How do you protect BSA/AML and fraud-model continuity through cutover?

- What did your last three banking modernization engagements actually cost compared to the original SOW?

- Who, by name and seniority, will be in the working sessions for the full engagement?

- Where would you tell us to keep the legacy core in a hollow-out rather than retire it?

Cost realities your CFO will ask about

How PiTech approaches legacy core modernization

PiTech defaults to coexistence for regulated mid-market banks because reporting continuity is the easiest commitment to keep and the hardest to undo when broken. Engagements ship the data foundation MDM, lineage, quality rules, source-to-target mapping, reconciliation evidence alongside the migration itself. Outcome reference: a Fortune 500 banking client’s SAS-to-IBM InfoSphere migration was compressed from 18 to under 11 months with 100% on-time milestone delivery, zero cost overruns, and 68% of data conflicts auto-resolved.

Frequently Asked Questions (FAQs)

What are the three core banking modernization strategies?

Which strategy is right for a mid-market bank?

Coexistence is usually the right default for regulated banks $5B–$50B in assets. It protects regulatory reporting and customer operations through the transition, allows the data foundation to be rebuilt domain by domain, and concentrates risk per wave rather than at a single cutover. Hollow-out fits when the legacy core is stable but constraining innovation; rip-and-replace fits very small institutions or well-capitalized banks with strong program discipline.

How long does legacy core modernization take?

Multi-year for full retirement of the legacy estate, but the program needs visible defensible wins inside the first 90 days to retain budget and board confidence. A focused first-domain win typically customer/account master data with MDM, lineage, and a first migration wave reconciled end-to-end is achievable in roughly 90 days regardless of which overall pattern is chosen. Duration depends primarily on asset size, regulatory complexity, and the condition of the data layer.

Can a bank modernize without a multi-year program?

What is the biggest hidden cost of core modernization?

The integration and data-foundation work source-to-target mapping, entity resolution, MDM, lineage, quality remediation, reporting rebuild and its run-rate over the next three years. Vendors typically exclude it from their license quotes, which is how a ‘reasonable’ modernization program turns into a wildly over-budget one. Get a specific dollar number for this bucket before signing the platform contract, not a percentage estimate.

How do we protect regulatory reporting through cutover?

Identify every regulatory report impacted by the source-system changes; map upstream fields across legacy and modern; recalculate disclosures in parallel for at least two cycles; retain audit evidence through the transition; lock reconciliation checkpoints before and after each migration wave. CECL, capital, stress-testing, BSA/AML, and Call Reports are the most exposed because they depend on the most data domains. Continuity is defensible only on governed data pipelines, not workflow automation over weak data.

What happens to BSA/AML and fraud models during modernization?

They must be treated as a first-class deliverable, not handed off. Inherited models need re-baselining against the new data architecture, alert thresholds re-validated on the post-migration data, lineage rebuilt so analysts can trace alerts to source, and case feedback re-wired into model retraining. Otherwise transaction monitoring quality degrades silently after cutover and the bank discovers it during the next examination, not the next monitoring report.

Should we modernize the core before or after AI investment?

Govern the data layer before scaling AI; you can run the two in parallel programs, but AI use cases will not reach production on ungoverned data. Most pilots fail for exactly this reason. The pragmatic sequence is to modernize the data foundation under one high-leverage domain (typically customer/account master data) while pursuing tightly scoped AI pilots that depend on that domain; then expand both together as governance matures across the estate.

What does 'AI-ready data platform' mean in practice?

A platform with governed data domains owned, defined, quality-controlled, lineage-backed plus a feature store, model inventory, monitoring, validation workflows, and policy controls aligned to SR 26-2 and the GenAI/agentic carve-out. AI-ready is not a marketing label on the data platform; it is the condition where new AI use cases can be onboarded with predictable governance and predictable quality. Without that condition, AI adoption is gated on case-by-case data heroics.

How do we measure modernization progress to the board?

Measure outcomes, not activity. Track governed-data coverage percentage by critical domain, reconciliation pass rates by wave, close-cycle days for CECL and regulatory reporting, AI use cases in production versus pilot, and examiner findings closed as a result of the program. ‘Applications migrated’ and ‘cloud adoption percentage’ are activity metrics that say little about whether the program is delivering value or surviving examination.