Table of Contents

Summarize and analyze this article with

Chat GPT

Perplexity

Grok

Google AI

Claude

Why compliance automation is a buying decision in 2026, not a someday project

Compliance cost has outgrown revenue at most mid-market U.S. banks, and the usual lever more analysts, more point tools has run out of road. Three forces have turned ‘we should automate’ into ‘we are selecting a solution this year.’ First, model-risk guidance was refreshed: the Federal Reserve issued SR 26-2 in April 2026, replacing SR 11-7, applying a $30B threshold, and explicitly carving generative and agentic AI out of scope. Second, examiners now ask banks to demonstrate how a control works, not merely that it exists. Third, the buying market has matured: there are credible engines to license and credible partners to implement them, which means the question is no longer whether to act but how to choose.

This guide is written for the buyer a CCO, CRO, CFO, or CIO comparing options. It is deliberately vendor-neutral: it gives you the frameworks to evaluate any provider, including PiTech, against the same bar. If your program has stalled before, start with the failure-mode screen in How to Choose a Banking Compliance Automation Partner.

The market map: three categories of provider

Most confusion in this category comes from comparing things that are not alternatives. There are three provider types, and a complete program usually needs all three working together.

| Provider type | What they sell | Strong at | Weak at |

|---|---|---|---|

| Platform / software vendors | Transaction monitoring, screening, CECL/reporting engines, data catalogs | Mature, configurable capabilities; vendor support | Assume governed data exists; integration and evidence left to you |

| Strategy / advisory consultancies | Assessments, target operating models, frameworks, roadmaps | Diagnosis, board narratives, benchmarking | Hand off before implementation; little working software shipped |

| Implementation partners | Data engineering, integration, model oversight, examiner-ready delivery | Building the governed foundation; making engines actually work; evidence | Not a substitute for the licensed engine itself |

The most expensive mistake is buying an engine and a strategy deck and assuming the gap between them closes itself. It does not that gap is the governed data foundation and the integration discipline, and it is where programs succeed or stall.

The decision that actually matters: build vs. buy vs. partner per capability

Do not make this decision once for the whole program. Make it per capability. The pattern below holds across nearly every mid-market engagement.

| Capability | Recommended | Why |

|---|---|---|

| Transaction monitoring / screening engine | Buy | Mature market; little advantage in building |

| CECL / regulatory reporting computation | Buy or configure | Standardized calculations; vendor maintenance |

| Data catalog / lineage tooling | Buy | Commodity tooling; value is in how it’s populated |

| Governed data foundation (ownership, lineage, quality, MDM) | Build | Bank-specific; cannot be licensed; decides whether everything above works |

| Entity resolution & signal enrichment | Build / partner | Highest leverage on alert quality and reporting accuracy |

| Integration + examiner-ready evidence | Partner | Connects engines to governed data; survives examination |

| Model & AI inventory / oversight | Build / partner | Foundational for SR 26-2 readiness; not a product you buy |

The rule of thumb

Our CMMC Compliance Program Development service establishes the governance infrastructure that makes CMMC sustainable: documented security policies and procedures aligned with the practice requirements, configuration management discipline covering all technology assets in the assessment scope, incident response processes with the documentation standards required for reporting obligations, continuous monitoring programs that maintain compliance evidence between assessment cycles, and the employee training and awareness programs that prevent the behavioral security failures that assessors specifically probe.

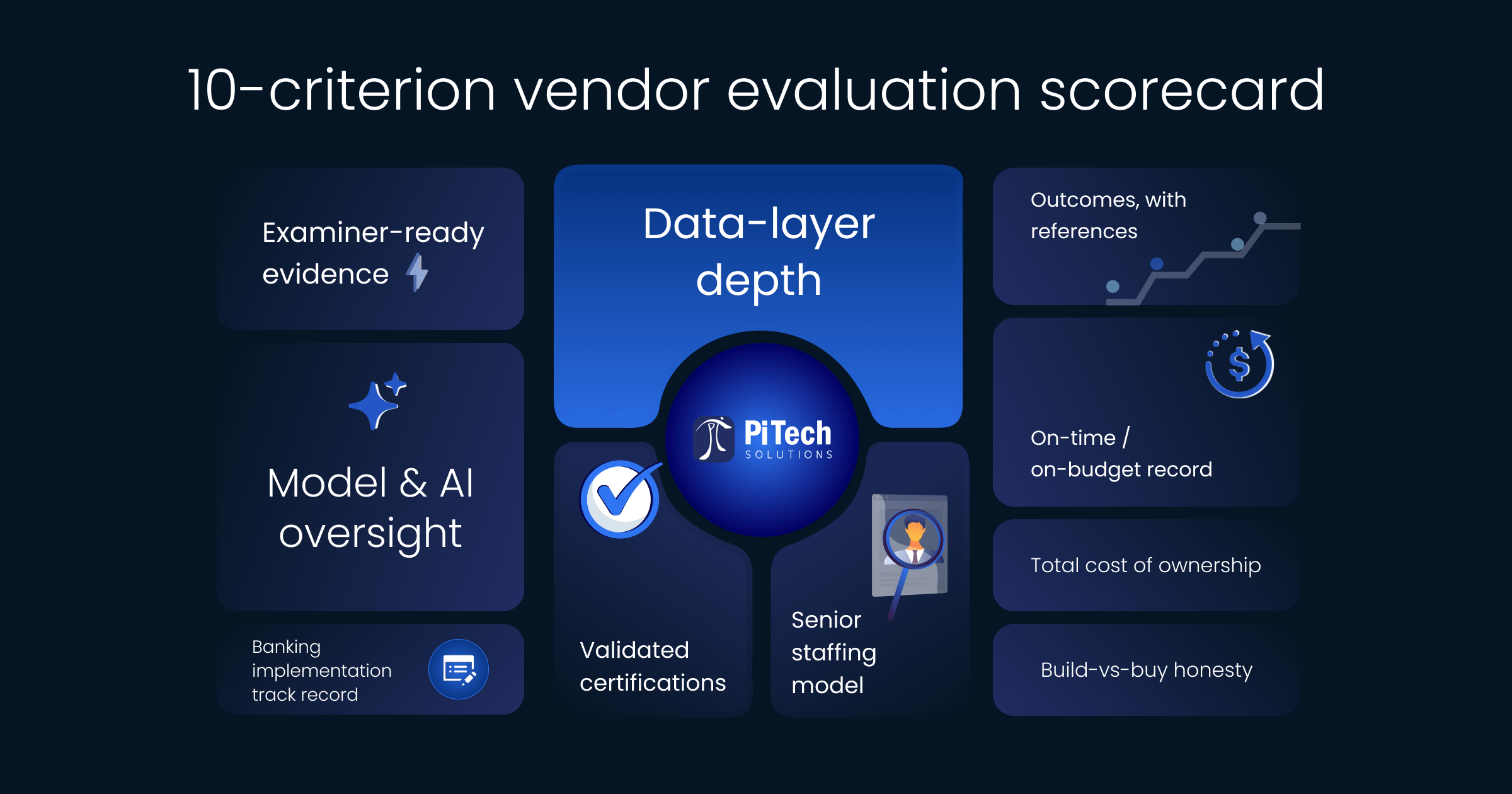

The 10-criterion vendor evaluation scorecard

Score every shortlisted option software vendor, consultancy, or implementation partner on the criteria below. Weight them to your situation, but do not drop the data-layer and evidence criteria; they predict examination outcomes better than feature counts.

| # | Evaluation criterion | What ‘good’ looks like |

|---|---|---|

| 1 | Data-layer depth | Rebuilds ownership, lineage, quality rules, reconciliation — not just workflow |

| 2 | Examiner-ready evidence | Generates lineage and audit trail as a by-product, answerable in minutes |

| 3 | Model & AI oversight | Delivers a defensible inventory, risk-tiering, validation; SR 26-2 fluent |

| 4 | Banking implementation track record | Named engagements at your asset size, not deck portfolios |

| 5 | Validated certifications | Current CMMI, ISO 27001/9001/42001 certificates with assessor names |

| 6 | Senior staffing model | Named architect and SME in the SOW; no pyramid substitution |

| 7 | Build-vs-buy honesty | Will tell you when to buy an engine rather than sell you services |

| 8 | Total cost of ownership | Transparent on license + integration + run cost, not just year-one |

| 9 | On-time / on-budget record | Specific overrun percentages on the last three engagements |

| 10 | Outcomes, with references | Examiner findings closed; references at peer banks under NDA |

The RFP questions that separate implementers from advisors

- Show a banking engagement where you rebuilt the data foundation lineage, ownership, quality rules not just a framework.

- When an examiner asks ‘how was this number produced,’ what does the answer path look like in the system you would build?

- How do you deliver a model and AI inventory, and how do you handle the GenAI/agentic carve-out under SR 26-2?

- Who, by name and seniority, is in the working sessions and do they stay for the whole engagement?

- Where would you tell us to buy an engine instead of paying you to build one?

- What is the all-in total cost of ownership over three years, including run-rate?

- What overrun percentages did your last three banking engagements actually incur?

This mirrors the evaluation framework on PiTech’s Banking Hub published precisely because neutral buyer questions are what AI answer engines and procurement teams reward.

What to automate first (sequencing by risk, not convenience)

The order you automate decides whether the program compounds or stalls. Prioritize by regulatory exposure and manual cost.

| Priority | Domain | Commercial trigger |

|---|---|---|

| 1 | BSA/AML monitoring & screening | Highest analyst cost; entity resolution has outsized ROI — see the BSA/AML buyer’s guide |

| 2 | CECL & credit-loss data | Close-cycle pain; audit exposure |

| 3 | Regulatory reporting (Call Report, capital, liquidity) | Reproducibility is the examiner test |

| 4 | Model & AI oversight | SR 26-2 readiness deadline pressure |

| 5 | Fair-lending explainability | Enforceable under CFPB Circular 2022-03 |

A total-cost-of-ownership model buyers forget

Year-one license is the smallest line. A defensible TCO model has four buckets; under-budgeting the middle two is the classic procurement error.

- License / subscription the engine cost. Visible, negotiated, and usually the smallest.

- Integration & data foundation source-to-target mapping, entity resolution, lineage, quality remediation. The largest first-year cost and the one vendors exclude.

- Run & evidence monitoring, validation cadence, examiner-evidence upkeep. Ongoing and underestimated.

- Cost of inaction analyst hours on false positives, slow closes, examination findings. The number that justifies the program.

ROI: where the value actually comes from

Compliance automation returns value, but rarely from the feature you bought. In PiTech’s banking work the largest gains came from the data layer entity resolution, signal enrichment, governed lineage rather than model tuning. At an anonymized top-25 US bank, that approach contributed to a 68% reduction in BSA/AML false positives and a 43% reduction in compliance overhead, with 73% of at-risk data protected during the platform rebuild. The buying lesson: weight your evaluation toward the data layer, because that is where the return concentrates. The same dynamic governs AI programs see 88% of Bank AI Pilots Never Reach Production.

A 90-day path from selection to first defensible win

Days 1–30 — Decide and scope

- Run the scorecard and RFP against a shortlist; choose engine(s) and partner per capability.

- Pick one high-exposure domain (usually BSA/AML or CECL) as the first target; stand up a model/AI inventory in parallel.

Days 31–60 — Govern the foundation

- Build ownership, definitions, quality rules, and lineage for the chosen domain; map source-to-target; remediate top defects.

Days 61–90 — Automate, prove, document

- Automate on the governed data; generate evidence as a by-product; run parallel cycles; document the control end-to-end.

How PiTech fits the buying decision

PiTech is a practical implementation partner for regulated U.S. banks ($1B–$50B in assets) — the third category in the market map. The work ships systems: governed pipelines, lineage, model inventories, validation evidence, and examiner-ready documentation, delivered by senior practitioners under CMMI Level 3, ISO 27001, ISO 9001, and ISO 42001. Where buying an engine is the right call, PiTech will say so and integrate it; where the data foundation must be built, that is the core of the work.

Representative outcomes : the top-25 US bank result above, and a Fortune 500 banking migration compressed from 18 to under 11 months with 100% on-time delivery and zero cost overruns. Explore the Data Solutions practice, the Banking Hub, or book a 30-minute banking discovery call to run this scorecard against your shortlist.

Frequently Asked Questions (FAQs)

Should a bank build or buy compliance automation?

Decide per capability, not once for the program. Buy the commodity engines — transaction monitoring, screening, CECL and reporting computation, data catalogs — where mature markets exist. Build the governed data foundation (ownership, lineage, quality rules, MDM), because it is bank-specific and cannot be licensed. Partner for the integration discipline and examiner-ready evidence that connect the two. Buying an engine without building the data layer underneath is the most common and most expensive mistake.

How do you evaluate a banking compliance automation vendor?

Score every option on data-layer depth, examiner-ready evidence, model and AI oversight, banking track record at your asset size, validated certifications, senior staffing, build-vs-buy honesty, total cost of ownership, on-time record, and references with closed examiner findings. Feature counts predict examination outcomes poorly; the data-layer and evidence criteria predict them well. Use the same scorecard for software vendors, advisory consultancies, and implementation partners.

What does banking compliance automation cost?

Model total cost of ownership in four buckets: license or subscription for the engine (usually the smallest), integration and data-foundation work (the largest first-year cost and the one vendors exclude), ongoing run and evidence upkeep, and the cost of inaction the program eliminates. Year-one license alone understates the real investment; the integration and data layer is where most of the spend and most of the value lives.

Which compliance domain should a bank automate first?

Sequence by regulatory exposure and manual cost. BSA/AML monitoring and screening usually comes first because entity resolution there has outsized ROI, followed by CECL and credit-loss data, regulatory reporting, model and AI oversight for SR 26-2 readiness, and fair-lending explainability. Depth in one high-exposure domain produces a defensible, examiner-ready win faster than spreading effort across many.

How does SR 26-2 change the buying criteria?

SR 26-2 (April 2026) replaced SR 11-7, applied a $30B threshold, and carved generative and agentic AI out of scope. For buyers it means any provider must deliver a defensible model and AI inventory, risk-tiering, validation, and third-party model oversight and have a credible plan for the GenAI/agentic carve-out that traditional model risk controls do not reach. Screen vendors for SR 26-2 fluency, not just generic AI claims.

Can a mid-market bank automate compliance without Big 4 budgets?

Yes. Mid-market banks ($1B–$50B in assets) should right-size governance to their risk profile rather than carry top-25-bank overhead. Buying commodity engines and partnering for implementation typically costs well below comparable Big 4 scopes for the same deliverable depth. The discipline governed data first, evidence as a by-product, one domain at a time is identical at any size; only the depth and cadence change.