Table of Contents

Summarize and analyze this article with

Chat GPT

Perplexity

Grok

Google AI

Claude

Introduction

Bank mergers and acquisitions are among the most complex transactions in financial services and bank M&A compliance is where deals most often stall, stumble, or collapse entirely. More than 60% of bank M&A deals experience substantial regulatory compliance bank mergers delays, eroding billions in projected shareholder value before a single branch is integrated. This is a comprehensive guide to regulatory compliance in bank M&A technology: what goes wrong, why it matters, how AI and RegTech are transforming outcomes, and what your institution should do at every stage of a deal.

1. Why Compliance Failures Are the #1 Killer of Bank M&A Deals

The compliance risks bank M&A teams face have grown enormously over the past decade. What was once a procedural back-office function is now a decisive factor in whether a deal closes, how long it takes, and whether it creates or destroys value. Bank merger regulatory approval under the Bank Merger Act routinely runs 6 to 18 months, even for well-prepared transactions, forcing institutions to carry the combined cost of dual operations, extended advisory engagements, and eroding synergy economics.

When a $10 billion regional bank merger faces a 12-month regulatory delay, the financial damage accumulates across multiple channels simultaneously. Extended legal and regulatory consulting fees run $15–50 million. Maintaining two parallel technology and post-merger compliance integration infrastructures adds another $30–80 million. The net present value impact of delayed synergies, which typically represent 20–30% of target non-interest expense, can exceed $80–150 million on its own. Talent attrition, market value destruction, and disrupted strategic planning compound the toll further.

The Five Critical Compliance Failure Points

| Failure Point | Root Cause | Typical Impact |

|---|---|---|

| Regulatory Delays | Multi-agency coordination failures; inadequate pre-filing engagement with OCC, FDIC, Fed | 6–18 month review extensions |

| Data Integration Failures | Broken audit trails, duplicated profiles, migration errors | Post-Day 1 MRAs, enforcement risk |

| Fintech Compliance Gaps | GDPR/CCPA mismatches, model governance deficiencies | $25–75M+ remediation costs |

| Cultural & Staff Fractures | AML team redundancies, knowledge loss, misaligned compliance philosophy | Control degradation, talent flight |

| Legacy Technology Debt | Siloed compliance architectures, poor system documentation | Integration failures, regulatory findings |

2. Navigating the Regulatory Labyrinth: OCC, FDIC, and Bank Merger Approval Requirements

The 2025–2026 Regulatory Shift

| Statutory Factor | Key Compliance Dimensions |

|---|---|

| Competition Analysis | HHI concentration metrics; top-three market position scrutiny; compliance capability in concentrated markets |

| Financial & Managerial Resources | Capital adequacy; risk management quality; compliance infrastructure sufficiency; integration track record |

| Future Prospects | Synergy projections; integration expense justification; management projection credibility |

| CRA Compliance Merger | CRA rating quality; community development effectiveness; disparate impact analysis |

| AML/BSA Effectiveness | SAR quality and timeliness; sanctions screening; customer due diligence adequacy |

| Financial Stability | Systemic risk; size, complexity, interconnectedness; cross-border supervisory coordination |

| Community Needs | Public interest standard; climate risk; diversity and inclusion; technology accessibility |

The OCC’s Technology Integration Expectations

A critical shift in the regulatory environment is the OCC’s heightened scrutiny of technology integration planning as a condition of merger approval. Understanding OCC FDIC merger approval requirements means recognizing that examiners now request detailed phased integration timelines, system consolidation strategies, risk mitigation plans, compliance continuity protocols, and resource commitments all before approval is granted. Institutions that treat integration planning as a post-approval activity do so at significant risk to both timeline and outcome.

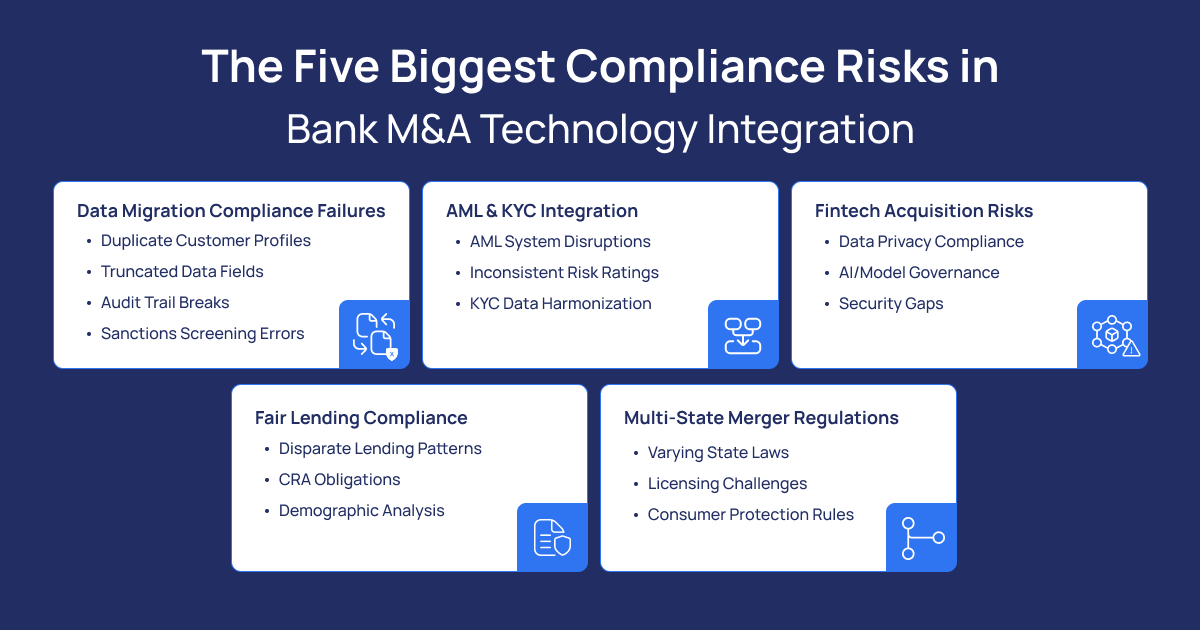

3. The Five Biggest Compliance Risks in Bank M&A Technology Integration

3.1 Data Migration Compliance Failures

The biggest regulatory risks in banking M&A are often hidden inside data migration. The migration of customer data across merging institutions is one of the highest-risk activities in any bank integration. The compliance implications of migration errors are far-reaching: broken audit trails, inconsistent customer risk profiles, incomplete transaction histories, and corrupted KYC documentation can all trigger regulatory findings that persist for years after nominal integration completion.

Common data migration compliance banking failure modes include customer profile duplication (which creates redundant and potentially conflicting risk assessments), data field truncation (which produces incomplete risk profiles and reporting errors), historical record corruption (which breaks audit trails required for regulatory examination), and sanctions list matching degradation (which creates potential OFAC violation exposure). Detection is frequently delayed because many failures are only discovered under regulatory examination long after the migration event that caused them.

3.2 AML/KYC Bank Acquisition Integration

Consolidating AML transaction monitoring systems from two institutions with different detection scenarios, alert thresholds, and case management workflows is technically complex and compliance-critical. The challenge of managing AML KYC bank acquisition integration is compounded by the transition period risk: when legacy systems may be partially decommissioned while unified systems are not yet fully calibrated, genuine suspicious activity detection can fail. Regulators take these windows extremely seriously.

The KYC challenge is equally significant in any post-merger compliance integration. Customer risk ratings assigned under different methodologies must be harmonized without creating systematic over- or under-assessment of risk. Data gaps revealed during harmonization require structured customer outreach programs. The combined institution must demonstrate to regulators that its KYC posture on Day 1 is as robust as each predecessor’s standalone posture, a standard that demands advanced technology support.

3.3 Fintech Acquisition Compliance Standards

Traditional bank-to-bank mergers present familiar compliance challenges. Fintech acquisition compliance introduces an entirely different risk profile. Fintechs typically operate with security frameworks, data governance practices, and model risk management programs built for speed and agility rather than bank-grade regulatory compliance. Understanding how fintech acquisition affects bank compliance standards is essential for any institution pursuing digital M&A.

Data privacy risks bank mergers are often the most immediately quantifiable exposure in fintech deals. Fintechs may have collected, shared, or monetized customer data under terms of service that do not meet GDPR, CCPA, or banking-specific data use requirements. Model governance is the longer-term challenge: AI and machine learning systems that form a fintech’s core value proposition must be retrofitted with comprehensive documentation, independent validation frameworks, and ongoing monitoring programs, a process that can take 18–36 months and cost tens of millions of dollars.

3.4 Fair Lending Compliance M&A Banking

Fair lending bank mergers compliance requires analysis of lending patterns across both predecessor portfolios simultaneously, a dataset that may encompass millions of loan applications across dozens of geographies, products, and demographic groups. Disparate impact patterns that were not apparent in either institution’s standalone analysis may become visible and actionable when viewed in aggregate. CRA compliance merger obligations add another layer: assessment area assignments, branch geographic coverage, and community development activity records must all be reconciled and verified before regulatory submission.

3.5 Multi-State Bank Merger Regulations

For institutions operating across multiple states, multi-state bank merger regulations extend compliance obligations to 50+ distinct regulatory frameworks with varying licensing requirements, consumer protection laws, UDAAP standards, and ongoing compliance obligations. Marketing materials, product terms, and customer-facing disclosures that were compliant in each institution’s existing footprint may require modification or replacement in the combined organization’s expanded service territory. The manual effort required to track, analyze, and document multi-state compliance obligations has historically been a significant source of both cost and delay.

4. AI and RegTech Solutions Transforming Bank M&A Compliance

4.1 AI for Bank Merger Compliance: From Weeks to Days

AI for bank merger compliance has fundamentally changed the economics and speed of due diligence. The compliance due diligence bank acquisition process previously required weeks of manual review across document populations of 40,000 pages or more. AI-powered document intelligence platforms now process the same volume in days, automatically identifying change-of-control clauses, regulatory obligations, data handling restrictions, and unusual risk allocation provisions directing human reviewers to the highest-priority items rather than requiring comprehensive reading of every document.

What AI tools detect regulatory violations in banking M&A documents? Leading platforms including LEGALFLY, Drooms AI, and SmartRoom employ large language models trained on legal and regulatory documents to flag non-compliant provisions, hidden liabilities, and enforcement indicators. These represent the core of modern AI compliance M&A banking capabilities.

| AI Due Diligence Capability | Compliance Application | Efficiency Gain |

|---|---|---|

| Document classification and extraction | Regulatory clause identification; obligation mapping | 70–80% review time reduction |

| Risk flagging and pattern detection | Non-compliant provisions; hidden liabilities; enforcement indicators | Consistent coverage across entire data room |

| Multilingual processing | Cross-border transaction support; international regulatory review | Eliminates translation bottlenecks |

| Change-of-control detection | Contract compliance; regulatory notification requirements | Automated versus manual search |

| Data privacy exposure assessment | GDPR/CCPA gap identification; fintech data practice review | Quantified risk versus qualitative estimate |

The critical discipline is treating AI as an advanced first-pass reviewer rather than a replacement for expert judgment. Institutions that build governance frameworks requiring human verification of AI outputs before informing board recommendations or regulatory submissions gain the efficiency benefits without the overreliance risk.

4.2 Real-Time Compliance Monitoring During Integration

The integration period represents the highest-risk window for compliance failures. The question “how do banks handle AML/KYC checks in post-merger integrations?” has a clear answer in 2025: through AI-powered dynamic KYC programs that continuously assess customer risk ratings across both predecessor populations, AML KYC bank acquisition transaction monitoring that consolidates detection scenarios with intelligent threshold calibration, and data lineage tools that maintain audit trail integrity across complex multi-system migration environments.

Industry data indicates that AI compliance M&A banking tools can reduce false positive rates in AML monitoring by up to 70% while maintaining or improving genuine suspicious activity detection, a double benefit that reduces operational cost while improving regulatory defensibility.

4.3 RegTech for Financial M&A: Regulatory Change Management

RegTech bank mergers solutions have matured into comprehensive platforms addressing the full compliance lifecycle. RegTech for financial M&A leaders like Compliance.ai monitor regulatory developments across 50+ jurisdictions simultaneously, delivering only content relevant to specific business activities and automatically mapping regulatory changes to internal policies and controls. For multi-state bank merger regulations, this capability eliminates the manual effort of tracking divergent state-level consumer protection requirements, licensing obligations, and reporting standards.

4.4 Predictive Compliance: How to Avoid Compliance Surprises on Day 1

How to avoid compliance surprises on Day 1 of a bank acquisition is one of the most frequently asked questions in banking M&A technology compliance. The answer lies in predictive risk identification—using machine learning models trained on historical merger approval data to anticipate regulatory concerns before they are raised. Applications include CRA and fair lending bank mergers outcome modeling that projects combined portfolio risk under different geographic and product configurations, competition analysis simulation, and early warning systems that identify emerging conduct risks in customer complaint data and operational metrics before they manifest in examination findings.

Institutions that invest in predictive compliance analytics can enter the regulatory review process with documented remediation plans for issues they have already identified and addressed a posture that materially improves both bank merger regulatory approval timeline and regulatory relationship quality.

5. The Human-AI Partnership: Redesigning Compliance Teams for M&A Success

Will my AML job be at risk during a bank merger? This question reflects genuine anxiety with tangible consequences. The answer is nuanced: AI for bank merger compliance is systematically automating routine transaction review, document analysis, and standard monitoring activities, but it is simultaneously creating demand for professionals with new, higher-value skill sets. Entry-level positions focused on manual processing are most susceptible to displacement. Senior analysts capable of AI system validation, complex investigation leadership, and regulatory relationship management are in growing demand across banking M&A technology compliance functions.

| Traditional Role (Declining) | Emerging Role (Growing) |

|---|---|

| Manual transaction review | AI system training, validation, and output interpretation |

| Document analysis and filing | Strategic risk assessment and regulatory navigation |

| Routine regulatory reporting | Complex investigation leadership |

| Standard compliance monitoring | Data literacy and AI-fluent compliance strategy |

| Data entry and reconciliation | Examination relationship management |

Cultural integration is a dimension that technology cannot address. Compliance teams from acquiring and target institutions bring different regulatory philosophies, different relationships with examiners, and different institutional practices that must be deliberately reconciled rather than simply combined. Proactive retention strategies are as important as any technology investment for achieving successful post-merger compliance integration.

6. The Business Case: ROI of AI and RegTech in Bank M&A

The financial case for investing in RegTech bank mergers capabilities before and during a deal is straightforward: the cost of inaction substantially exceeds the cost of investment. A single avoided MRA can save $50–150 million in remediation costs and regulatory relationship damage. Each month of bank merger regulatory approval timeline acceleration is worth $10–30 million in delay cost avoidance and $40–100 million in NPV from earlier synergy realization.

| Benefit Category | Quantification Method | Typical Value |

|---|---|---|

| MRA Prevention | Avoided remediation costs per MRA prevented | $50–150M per MRA |

| Timeline Acceleration | Monthly delay cost reduction per month gained | $10–30M per month |

| Synergy Capture | NPV of earlier synergy realization | $40–100M per 6-month acceleration |

| Talent Efficiency | Manual effort reduction (60–70%) across compliance team | Ongoing operational advantage |

| Regulatory Credibility | Improved examination relationships and approval predictability | Reduced deal uncertainty premium |

Institutions that treat M&A as an opportunity to accelerate enterprise banking M&A technology compliance modernization gain competitive advantages that extend well beyond any individual deal. Superior compliance capability becomes a differentiator in regulatory relationships, a source of deal certainty that commands valuation premiums, and a platform for ongoing operational efficiency.

7. Implementation Roadmap: From Pre-Deal Assessment to Day 1 Readiness

Phase 1: Compliance Due Diligence Bank Acquisition

Phase 2: Integration Planning and Regulatory Engagement

Phase 3: Cutover and Post-Merger Optimization

The controlled transition to combined systems requires maintained rollback capability, comprehensive validation testing against defined compliance metrics, and structured exception resolution protocols. Ongoing post-merger compliance integration optimization encompasses model monitoring and refinement, examination preparation and response management, and systematic capture of lessons learned for organizational knowledge building.

| Phase | Timeline | Key Compliance Activities |

|---|---|---|

| Pre-Deal Diligence | Pre-announcement | Compliance architecture review; data quality assessment; regulatory risk profiling |

| Regulatory Filing | Months -3 to 0 | Pre-clearance engagement; MRA remediation; integration planning finalization |

| Parallel Operation | Months 0 to 6-12 | System coexistence; output comparison; customer migration validation |

| Cutover Execution | Weeks 1-4 post-cutover | Controlled transition; rollback capability; comprehensive validation |

| Post-Merger Optimization | Ongoing | Model refinement; examination preparation; organizational learning |

8. The Future of Bank M&A Compliance Technology

The trajectory of banking M&A technology compliance points toward three transformative developments over the next three to five years. Embedded compliance AI agents with autonomous decision-making capabilities within defined parameters will replace manual approval workflows for routine compliance determinations. Real-time regulatory reporting through API-based continuous data provision will replace periodic submission cycles, creating perpetual examination readiness. Cross-border regulatory harmonization frameworks will reduce the complexity of international bank M&A by creating standardized data exchange and supervisory coordination protocols.

For bank leadership, the strategic imperative is clear: institutions that invest in AI for bank merger compliance and RegTech for financial M&A capabilities today are not merely preparing for individual transactions. They are building the regulatory credibility, operational efficiency, and talent infrastructure that determines which institutions can pursue M&A as a growth strategy and which are effectively excluded by compliance risks bank M&A. The compliance valley the gap between regulatory expectation and institutional capability is where bank M&A deals die. AI and RegTech are the bridge across it.

Ready to De-Risk Your Next Bank M&A Transaction?

Regulatory delays are not inevitable. They are preventable with the right compliance architecture, AI-enabled due diligence, and structured integration governance.

If your institution is preparing for an acquisition, responding to regulatory scrutiny, or modernising compliance technology, the right partner can determine whether your deal accelerates or stalls.

Pitech helps financial institutions strengthen compliance readiness, streamline regulatory approval, and implement AI and RegTech solutions that protect deal value from Day 0 through post-merger optimization.

Do not let compliance risk dictate your growth strategy.

Key Takeaways

- More than 60% of bank M&A deals face compliance risks bank M&A-related delays costing $195–520 million per year of delay for a $10 billion transaction.

- AML compliance in bank mergers has become the primary single source of regulatory delay and deal failure—as the TD-First Horizon case made clear at the $13.4 billion scale.

- AI for bank merger compliance compresses 40,000-page document review from weeks to days, with 70–80% reduction in review time and consistent coverage across entire data rooms.

- Data migration compliance banking particularly the protection of audit trail integrity, customer profile consistency, and KYC completeness, represents the highest-risk activity in any post-merger compliance integration and requires dedicated AI-powered governance controls.

- Fintech acquisition compliance introduces qualitatively different risks: GDPR/CCPA exposure (data privacy risks bank mergers), model governance deficiencies, and security posture mismatches that require specialized assessment.

- Multi-state bank merger regulations and fair lending bank mergers obligations require AI-powered mapping tools to manage 50+ jurisdictions without prohibitive manual effort.

- The ROI of RegTech bank mergers investment is measurable: $50–150M per avoided MRA, $10–30M per month of timeline acceleration, and $40–100M per six months of accelerated synergy realization.

Frequently Asked Questions (FAQs)

How can AI help with compliance solutions for banking regulations during mergers?

AI automates document review, clause detection, AML risk identification, and regulatory obligation mapping. It reduces manual effort by 60 to 80 percent and accelerates bank merger regulatory approval. AI also supports predictive risk modelling and real-time monitoring during post-merger compliance integration, helping institutions remediate issues before regulators raise them.

What are the biggest regulatory risks in bank M&A data migration?

Key risks include broken audit trails, duplicate customer records, incomplete KYC data, corrupted transaction histories, and degraded sanctions screening. These failures often trigger post-Day 1 MRAs. Data migration compliance banking must prioritise audit integrity and customer risk consistency.

How do banks handle AML/KYC checks in post-merger integrations?

Banks run parallel AML monitoring systems during transition, harmonise customer risk rating methodologies, and recalibrate alert thresholds. AI compliance M&A banking tools reduce false positives while preserving detection accuracy. Regulators expect Day 1 AML posture to be equal to or stronger than both legacy institutions.

What causes delays in bank merger regulatory approvals?

Delays typically stem from AML weaknesses, unresolved MRAs, competition concerns, incomplete integration planning, and insufficient pre-filing engagement with OCC, FDIC, or the Federal Reserve. Multi-agency coordination gaps extend review timelines.

How to avoid compliance surprises on Day 1 of a bank acquisition?

Conduct deep compliance due diligence before signing, validate data migration plans, remediate existing MRAs, and use predictive analytics to surface hidden risks. Early regulator engagement significantly reduces unexpected objections.