Table of Contents

Summarize and analyze this article with

Chat GPT

Perplexity

Grok

Google AI

Claude

Introduction

Nearly 70% of banking mergers fail to deliver expected value, and the root cause is rarely deal strategy. Instead, failure emerges from tech migration bank mergers execution. When systems fail to integrate, projected synergies collapse, costs rise, and regulators intervene.

Recent industry research shows that technology issues now account for a large share of post-deal delays, with many integrations running 50 to 100 percent over budget and slipping more than 60 percent beyond timelines. As consolidation accelerates through 2025 and into 2026, banks must treat bank merger IT integration as the core deal driver rather than a back-office task.

This article explains the real risks, modern solutions, and proven roadmap for successful core banking migration M&A and long-term banking technology consolidation.

Why Technology Now Determines Bank Merger Outcomes

Market pressure, digital competition, and regulatory scrutiny are reshaping consolidation strategy. According to recent industry analysis from Deloitte, banks increasingly pursue mergers to fund digital transformation and cloud modernization rather than only expand deposits or geography. Technology therefore becomes the primary integration battlefield.

Poor planning creates cascading failures. Legacy incompatibility blocks data sharing. Fragmented governance slows approvals. Customer-facing outages damage trust. These failures explain why analysts warn that integration risk can erase 15 to 30 percent expected IT cost synergies.

For banks working with transformation partners such as PiTech and implementing early architectural alignment significantly reduces post-merger disruption and accelerates value realization.

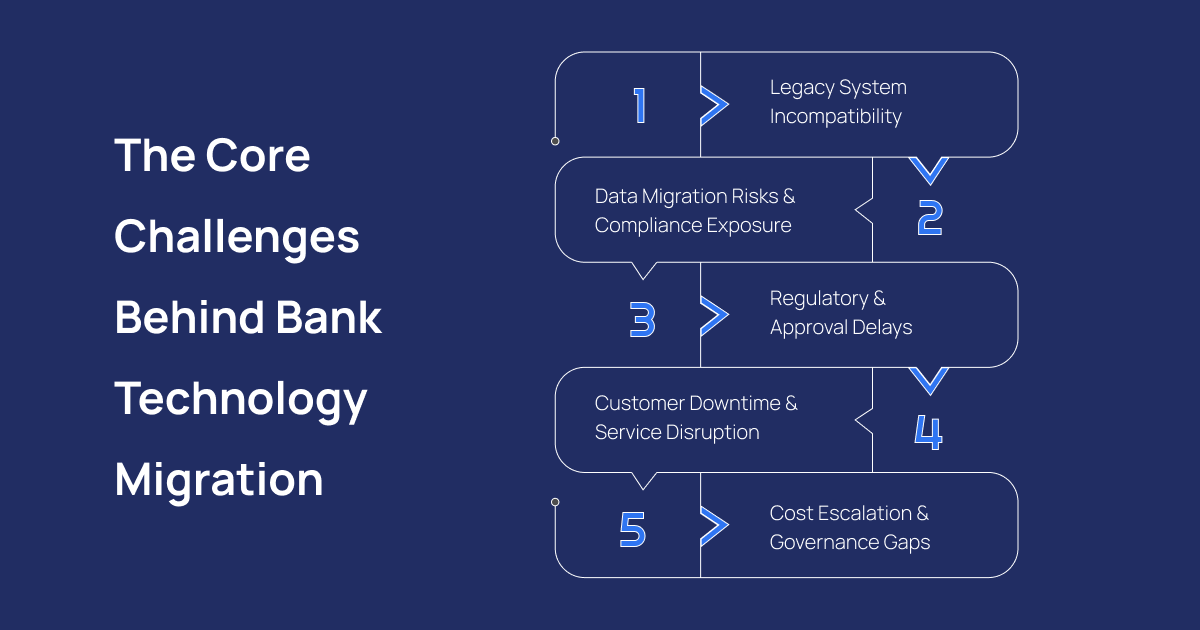

The Core Challenges Behind Bank Technology Migration

Legacy System Incompatibility

Many acquisitions still involve decades-old cores. Reverse engineering undocumented logic can take six to twelve months. This makes legacy system migration banking the first major blocker.

Industry research highlights that incompatible architectures remain one of the primary causes of failed integrations. Without a unified bank acquisition tech strategy, banks struggle to standardize products, reporting, and compliance workflows.

Data Migration Risks and Compliance Exposure

Data is the real asset in modern deals. Studies note that incomplete mapping, duplicate customer identities, and broken audit trails create severe regulatory exposure. Large integrations may process billions of records, making data migration challenges mergers a top risk category.

Secure reconciliation, automated validation, and staged post-merger system integration are now essential to prevent customer churn and compliance penalties.

Regulatory and Approval Delays

Supervisory bodies closely evaluate IT readiness before approving consolidation. Weak cyber controls, poor resiliency, or unclear migration governance can delay deals by six to eighteen months. This makes regulatory tech migration banking a strategic planning priority rather than a final checkpoint.

Customer Downtime and Service Disruption

Outages remain the most visible failure. Big-bang cutovers often trigger payment failures, login errors, or missing balances. To protect trust, banks now prioritize zero downtime banking migration using phased releases, parallel environments, and real-time monitoring.

Cost Escalation and Governance Gaps

Modern Technology Strategies That Reduce Migration Risk

Cloud-Led Integration and Platform Consolidation

Cloud adoption is accelerating across global banking. Analysts expect most new core deployments after 2026 to run on hybrid or public cloud infrastructure. Structured cloud migration bank M&A enables scalable environments, faster testing, and improved disaster recovery.

AI-Driven Data Mapping and Testing

Phased Core Transformation Instead of Big-Bang Replacement

Leading institutions avoid single-day conversions. Instead, they separate channels, payments, and lending into modular migration waves. This staged core banking migration M&A approach maintains service continuity while enabling gradual modernization.

A Practical Roadmap for Successful Bank Merger IT Integration

1. Define a Unified Technology Blueprint Early

Integration planning must begin during due diligence. Banks should map architectures, data models, and vendor contracts before deal closure. This reduces uncertainty in bank merger IT integration and improves regulatory confidence.

2. Build a Dedicated Integration Governance Office

3. Execute Parallel Data Validation and Testing

Continuous reconciliation prevents corruption and audit failures. Automated controls address the most severe data migration challenges mergers before customer exposure.

4. Prioritize Customer Experience Protection

Communication, fallback systems, and real-time monitoring protect trust during zero downtime banking migration. Customer-first planning now defines successful post-merger system integration.

5. Accelerate Value Through Cloud and AI

Combining cloud migration bank M&A with AI assisted bank mergers shortens timelines and unlocks analytics-driven cross-sell opportunities. This turns integration from cost center to growth engine.

Banks seeking structured execution often engage transformation specialists such as PiTech to align compliance, architecture, and delivery under a single roadmap.

Key Industry Trends Shaping Bank M&A Technology in 2026

Several shifts are redefining consolidation success:

- Digital capability is now a primary merger motive rather than branch expansion.

- Data governance and cybersecurity receive heavier regulatory scrutiny each year.

- AI adoption in migration testing and operational monitoring is rapidly expanding.

- Cloud-native cores are replacing monolithic systems across new integrations.

- Customer experience metrics increasingly determine merger approval and valuation.

The institutions prioritizing data architecture and digital platforms achieve faster synergy realization and lower integration failure rates.

The Strategic Opportunity Hidden Inside Technology Consolidation

Despite the risks, successful banking technology consolidation creates lasting competitive advantage. Unified platforms enable real-time analytics, personalized services, and lower operating costs. More importantly, they position banks for open banking ecosystems, embedded finance, and AI-driven decisioning expected to dominate beyond 2026.

Technology migration is therefore not only an operational hurdle. It is the defining moment that determines whether a merger delivers transformation or becomes an expensive distraction.

Conclusion:

Bank consolidation is accelerating, but only disciplined execution delivers value. Rising complexity, strict regulation, and fragile legacy environments make tech migration bank mergers the most critical phase of any deal. Institutions that invest early in governance, cloud readiness, AI automation, and customer-safe migration strategies consistently outperform peers in cost control and integration speed.

As the industry moves deeper into digital-first banking, bank merger IT integration will decide which mergers succeed and which fail. Banks that treat core banking migration M&A and long-term banking technology consolidation as strategic transformation programs rather than IT projects will lead the next decade of financial services innovation.

Key Takeaways

- Nearly 70% of bank mergers underperform, largely due to failed tech migration rather than poor deal strategy.

- Legacy system incompatibility and data migration risks are the primary causes of delays, cost overruns, and compliance exposure.

- Technology integration can exceed budgets by 50–100% without strong governance and early architectural alignment.

- Regulators now scrutinise cybersecurity, resilience, and data governance before approving consolidation.

- Cloud-led platforms and AI-assisted migration significantly reduce integration risk and improve execution speed.

- Banks that treat IT integration as a strategic transformation programme, not a technical task, gain long-term competitive advantage.

Frequently Asked Questions (FAQs)

What are the biggest tech migration failures in recent bank mergers?

Recent high-profile issues include M&T Bank’s acquisition of People’s United Financial, where customers were locked out of accounts due to security flagging problems. Truist Financial’s merger faced challenges migrating seven million customers across 100-plus software applications. These failures typically stem from underestimating legacy system complexity and inadequate testing.

How do banks migrate core systems during M&A without downtime?

Banks use parallel run strategies where old and new systems operate simultaneously. This doubles costs but protects 24/7 customer access. Component-based replacement, migrating one function at a time, reduces risk. Active-active configurations allow true co-existence with mirrored requests and calls.

What legacy system challenges arise in bank acquisitions?

Eighty-one percent of banking leaders cite legacy systems as a major hurdle. Challenges include COBOL code that few developers understand, batch processing that prevents real-time updates, undocumented custom logic requiring months to reverse-engineer, and limited API support that blocks modern integrations.

How to plan technology integration for bank mergers?

Start before the deal closes. Bring tech leaders into the process early. Map business processes before touching systems. Form a governance team with clear data ownership. Automate every migration step. Conduct repeated test migrations and dry runs. Establish a unified architecture team to prevent siloed decisions.

What is the timeline for full IT integration post-bank merger?

Core banking migration typically takes one to two years with modern approaches, down from multi-year initiatives of the past. However, regulatory approval delays can add six to eighteen months. The first year after close has the most significant impact on ultimate success or failure.