Table of Contents

Summarize and analyze this article with

Chat GPT

Perplexity

Grok

Google AI

Claude

Introduction

The banking sector in the United States has witnessed unprecedented consolidation over the past two decades. Regional banks are acquiring community institutions, while larger players continue their strategic expansion through mergers and acquisitions. Yet behind every successful bank merger lies a critical component that often determines whether the deal creates value or destroys it: IT due diligence.

When two financial institutions come together, they’re merging complex technology ecosystems built over decades, each with its own legacy systems, security protocols, vendor relationships, and regulatory compliance frameworks. The stakes couldn’t be higher. A single overlooked vulnerability in a technology audit for bank acquisitions can expose the combined entity to cybersecurity breaches, regulatory penalties, operational disruptions, and customer attrition that can wipe out the anticipated synergies of the deal.

This comprehensive guide explores the multifaceted world of bank M&A due diligence, providing actionable insights for executives, IT leaders, compliance officers, and advisors navigating these complex transactions in the American banking landscape.

Understanding the Critical Role of IT Due Diligence in Banking M&A

Why IT Due Diligence Makes or Breaks Banking Deals

The consequences of inadequate bank M&A due diligence are severe and well-documented.

Banks have discovered post-acquisition that core banking systems are incompatible, requiring complete replacement at costs exceeding initial projections by hundreds of millions of dollars. Others have inherited cybersecurity vulnerabilities that led to data breaches within months of closing.

Banking regulators, including the OCC, Federal Reserve, and FDIC scrutinize technology risk management with increasing intensity. They expect acquiring institutions to thoroughly understand the IT risks in banking mergers USA before receiving approval to proceed. Regulators have delayed or even denied merger applications due to concerns about the acquiring bank’s ability to successfully integrate technology systems while maintaining operational resilience.

The Evolution of Technology Risk in Banking M&A

Today’s bank mergers IT landscape bears little resemblance to that of even a decade ago.

Cloud computing has moved from experimental to mainstream. Artificial intelligence powers everything from fraud detection to customer service. Open banking APIs connect financial institutions to third-party fintech providers. Cybercriminals have become more sophisticated, with ransomware attacks specifically targeting financial institutions.

This evolution means that your bank M&A IT due diligence checklist must address modern technology considerations alongside traditional infrastructure assessments. You need to understand cloud architectures, API security, AI model governance, and third-party technology ecosystems.

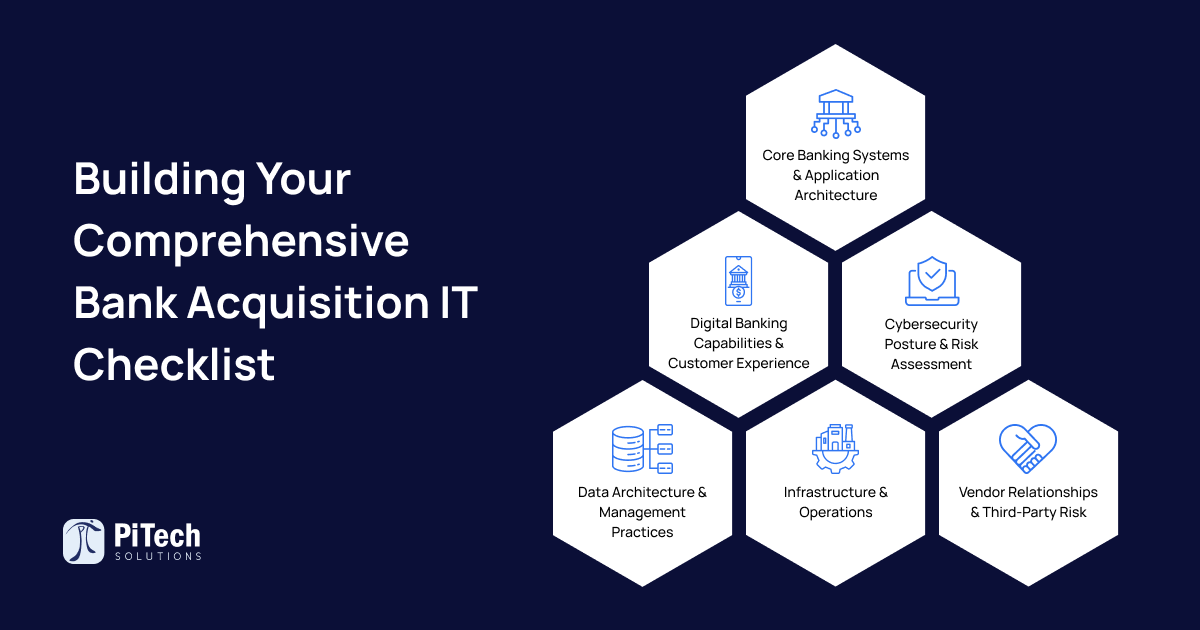

Building Your Comprehensive Bank Acquisition IT Checklist

Core Banking Systems and Application Architecture

The heart of any bank’s technology infrastructure is its core banking system.

Understanding the target institution’s core platform, version, customization level, and integration points is paramount. You need to determine whether the systems can coexist during a transition period or if immediate migration is necessary.

Many regional banks still operate on legacy platforms that may be decades old, with customizations that make upgrades or migrations extraordinarily complex. This is where thorough assessment of application risks bank deals becomes critical.

Key questions to answer:

- What core banking platform does the target use, and which version?

- How heavily customized is the system from the vendor's standard offering?

- What are the licensing costs and contract terms?

- How many interfaces connect the core system to other applications?

Banks often discover they’ve inherited hundreds of applications, many redundant or poorly documented. Understanding these application risks bank deals early allows for better synergy planning IT M&A.

Digital Banking Capabilities and Customer Experience

Digital banking capabilities require special attention in today’s market. With customers expecting seamless experiences, incompatible digital platforms can trigger customer attrition immediately following a merger announcement.

Assess the target’s digital banking platform, mobile app functionality, API architecture, and customer adoption rates as part of your M&A technology audit.

Critical digital banking elements to evaluate:

- Mobile banking app features, ratings, and usage statistics

- Online banking platform capabilities and user experience

- Payment processing systems including mobile wallets and P2P transfers

- Customer authentication methods and security features

- Integration with third-party fintech services

Cybersecurity Posture and Risk Assessment

Cybersecurity represents one of the most critical areas in financial M&A cybersecurity assessment.

You’re inheriting the target bank’s vulnerabilities, threat landscape, and potential exposure to cyberattacks. A thorough cybersecurity assessment should examine multiple dimensions of the target’s security program as part of a comprehensive banking IT risks evaluation.

Start with the security framework and governance structure:

Does the target institution follow recognized frameworks like NIST, ISO 27001, or the FFIEC Cybersecurity Assessment Tool? Who oversees cybersecurity at the board and management levels?

Examine technical security controls:

What endpoint protection solutions are deployed? How is network segmentation implemented? What intrusion detection and prevention systems are in place?

Review the incident history:

Has the target experienced any security breaches, ransomware attacks, or significant security incidents? How were they handled?

Understanding financial M&A cybersecurity risks early allows you to price the deal appropriately and plan for necessary security investments.

Data Architecture and Management Practices

Data is the lifeblood of modern banking, and secure data integration bank M&A requires deep understanding of how the target institution manages its data assets.

Examine the data architecture M&A banking across multiple dimensions. Where does customer data reside? How many databases exist? What data governance policies are in place?

Key data considerations include:

- Customer data repositories and master data management practices

- Data warehousing and business intelligence infrastructure

- Data retention and archival policies

- Data privacy controls and compliance with regulations like GLBA

- Data backup and disaster recovery processes

Poor data quality can undermine integration efforts and create compliance headaches. Secure data integration bank M&A becomes even more complex when institutions use different data models. Mapping customer data from one system to another while maintaining data integrity requires meticulous planning as part of your US bank acquisition IT checklist.

Infrastructure and Operations

The underlying technology infrastructure determines operational resilience and scalability.

Assess the target’s infrastructure across these areas:

Data centers: Does the target own its data centers or use colocation facilities? What is the age and condition of the infrastructure?

Cloud adoption: Has the target migrated workloads to public cloud platforms like AWS, Azure, or Google Cloud? Which applications run in the cloud versus on-premise?

Network architecture: How is the network designed and segmented? What bandwidth capacity exists?

IT operations: How are IT operations managed and monitored? What incident management processes exist?

Understanding infrastructure capabilities helps you plan secure IT integration bank activities and identify necessary investments.

Vendor Relationships and Third-Party Risk

Modern banks rely on hundreds of third-party vendors for technology services.

A comprehensive M&A technology audit must examine the target’s vendor ecosystem in detail, including thorough software contracts M&A review.

Review each significant vendor relationship:

- What services does the vendor provide?

- What are the contract terms, including length, renewal provisions, and termination clauses?

- What are the costs, including license fees, maintenance, and support?

- How financially stable is the vendor?

Pay particular attention to change-of-control provisions in vendor contracts during your software contracts M&A review. Some vendors include clauses that allow them to renegotiate terms following a merger. These provisions can significantly impact your cost assumptions, making IT budget validation in mergers essential.

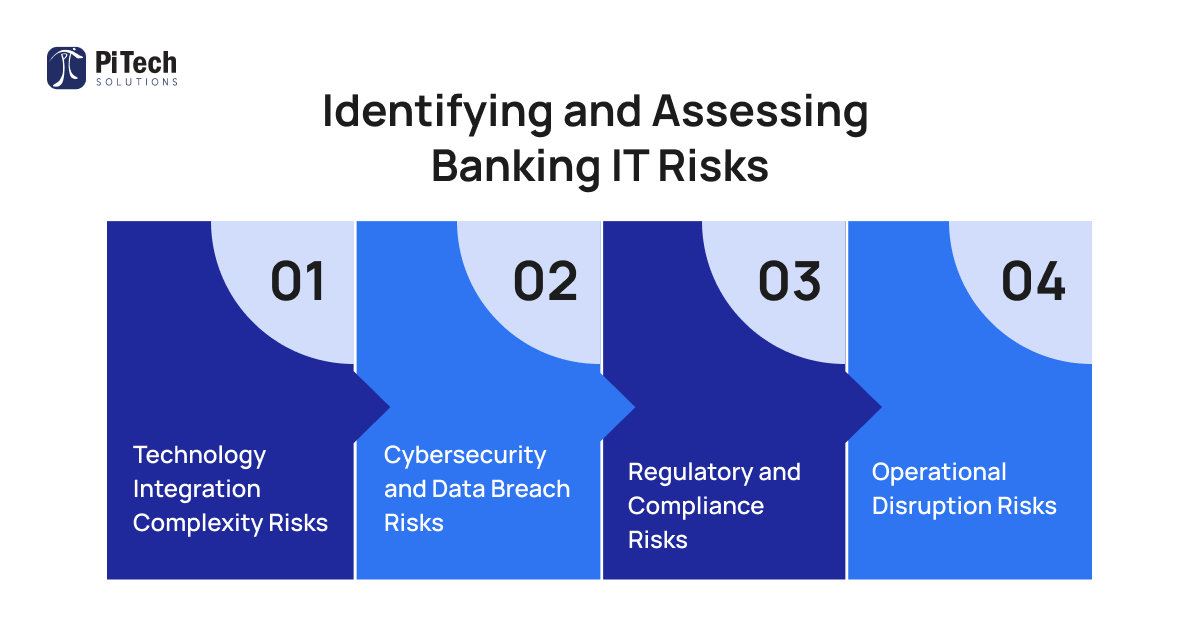

Identifying and Assessing Banking IT Risks

Risk identification and assessment form the core of bank M&A due diligence. The goal is to understand the banking IT risks thoroughly so you can price them appropriately and make informed decisions.

Technology Integration Complexity Risks

Assess integration complexity across several dimensions:

Technical compatibility between systems, programming languages in use, availability of integration tools, documentation quality, and the need for data transformation.

The integration approach dramatically impacts risk. Effective synergy planning IT M&A must account for these complexities.

Cybersecurity and Data Breach Risks

Inheriting cybersecurity vulnerabilities can expose your institution to devastating consequences.

During the due diligence period, you’re operating with limited visibility into the target’s security posture.

Focus on risk indicators:

Security incident history, vulnerability management practices, patch management processes, privileged access controls, third-party security assessments, and cyber insurance coverage.

Consider whether the target has suffered any unreported breaches. Post-acquisition discovery of a breach can result in notification obligations, regulatory penalties, litigation, and reputational damage.

Regulatory and Compliance Risks

Key regulatory risk areas include:

Information security program deficiencies, BSA/AML system gaps, consumer protection issues in digital channels, operational resilience weaknesses, and third-party risk management shortcomings.

Some institutions have discovered the target was operating under informal regulatory agreements requiring significant unexpected technology investments that impact IT budget validation in mergers.

Operational Disruption Risks

M&A creates inherent operational risks even when integration is well-planned.

System migrations and integrations always carry some risk of disruption. Customer-facing services might experience outages. Data integrity issues might arise during migration.

Assess the target's operational resilience:

How robust are business continuity and disaster recovery plans? What testing has been performed?

Consider the timing and sequencing of integration activities. This is where comprehensive synergy planning IT M&A makes the difference.

Leveraging AI Tools for M&A IT Assessment

Artificial intelligence is transforming how institutions conduct IT due diligence, enabling more thorough assessments in compressed timeframes.

Automated Code Analysis and Technical Debt Assessment

- Outdated programming languages and frameworks

- Known security vulnerabilities in code libraries

- Code complexity metrics that indicate maintenance challenges

- Duplicated code that suggests inefficient development practices

Document Analysis and Contract Review

Natural language processing algorithms can review thousands of vendor contracts, technical documentation, and policy documents in hours rather than weeks.

AI-powered document analysis can:

- Extract key terms from vendor contracts including pricing and termination clauses

- Identify inconsistencies between documented policies and regulatory requirements

- Summarize technical architecture documents

- Flag potential compliance gaps in documentation

This capability is valuable given the volume of documentation in bank mergers IT transactions. Human reviewers can focus on the most critical issues identified by AI tools for M&A IT assessment, making software contracts M&A review more efficient.

Data Quality and Anomaly Detection

Machine learning algorithms excel at identifying data quality issues and anomalies.

AI-powered data analysis can:

Assess customer data completeness and accuracy, identify unusual patterns that might indicate data integrity issues, detect potential data duplication, and evaluate data governance maturity.

Understanding data quality issues before integration prevents downstream problems, supporting better data architecture M&A banking decisions.

Cybersecurity Threat Intelligence

Best Practices for Conducting Effective IT Due Diligence

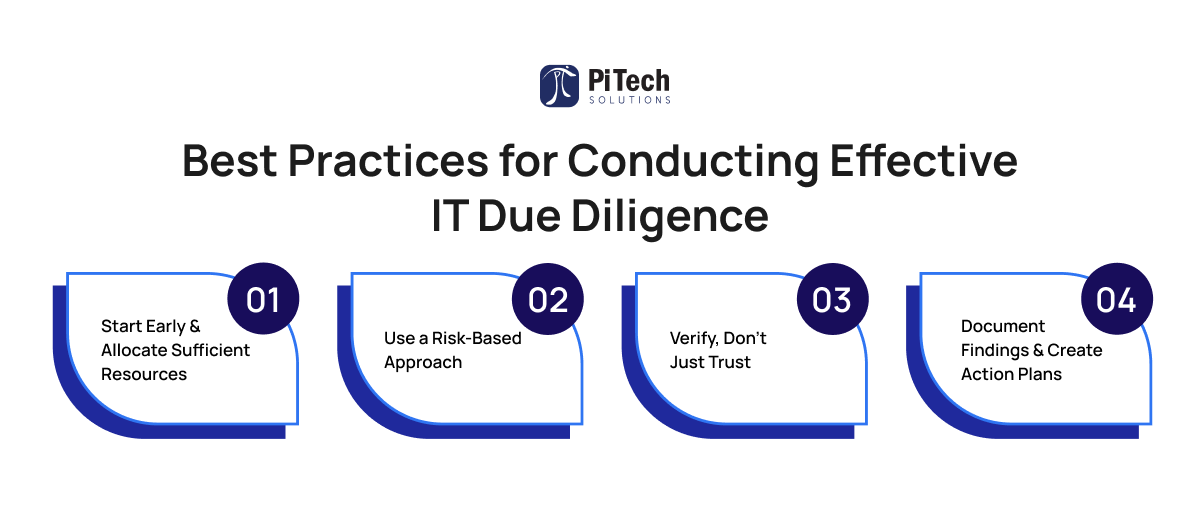

Experience from hundreds of banking M&A transactions has yielded proven practices that improve bank M&A due diligence effectiveness.

Start Early and Allocate Sufficient Resources

IT due diligence requires time and expertise. Starting late or under-resourcing leads to superficial assessments that miss critical issues.

Begin IT due diligence in parallel with financial and legal reviews. Allocate experienced technology professionals who understand banking systems. Consider engaging specialized consultants.

Create a detailed project plan with specific deliverables. Don’t assume you can complete comprehensive bank M&A due diligence in just a few weeks. Proper IT budget validation mergers require adequate time and resources.

Use a Risk-Based Approach

You can’t examine everything in equal depth, so prioritize based on risk and materiality.

Focus intensive efforts on:

Core banking systems and critical applications, cybersecurity controls and incident history, regulatory compliance areas with known challenges, and vendor relationships that represent significant costs.

This approach ensures your US bank acquisition IT checklist focuses on what matters most.

Verify, Don't Just Trust

Management representations provide valuable information, but verification is essential.

Request evidence supporting key assertions. If management claims robust disaster recovery capabilities, ask to see recent test results.

Look for consistency between what management says and what documentation shows. Discrepancies might indicate gaps representing potential banking IT risks.

Document Findings and Create Action Plans

Thorough documentation serves multiple purposes during and after the transaction.

Your documentation should include:

Detailed findings organized by risk category and severity, supporting evidence and data sources, impact assessments quantifying potential costs, recommended mitigation strategies, and action plans with timelines.

This documentation informs deal pricing, regulatory filings, integration planning, and supports effective synergy planning IT M&A.

Navigating Secure IT Integration Bank

Developing a Comprehensive Data Integration Strategy

Successful data integration starts with clear strategy and planning before the actual migration begins.

Your strategy should address:

Which systems will be integrated immediately versus later, how customer data will be consolidated and deduplicated, what data quality standards must be met, how data security will be maintained, and what validation steps will ensure data integrity.

Different data types may require different approaches. Understanding data architecture M&A banking helps inform these decisions.

Implementing Security Controls for Data in Transit

Data is most vulnerable during migration and integration activities.

Implement robust security controls:

Encrypt all data transfers between systems, use secure file transfer protocols, implement strict access controls limiting who can access data during migration, log all data access activities, and monitor for anomalous data access patterns.

Consider the physical and logical location of data during integration. How will you ensure they meet the same security standards as production systems?

Managing the Human Element of Data Integration

Technology isn’t the only challenge in secure IT integration bank—people and processes matter enormously.

Staff from both institutions need clear roles and responsibilities during integration. Who validates data quality? Who resolves discrepancies?

Provide training on new data management processes. Employees need to understand how to access and use customer data in the combined institution’s systems.

Create communication plans for addressing customer inquiries about their data.

Regulatory Considerations in Banking M&A IT Due Diligence

Regulators maintain intense focus on technology risk management in bank mergers and IT transactions.

Understanding Regulatory Expectations

Banking regulators expect acquiring institutions to demonstrate thorough understanding of technology risks before they approve mergers.

The FFIEC provides guidance on technology service provider management, information security, and business continuity. Regulators expect institutions to apply these standards when evaluating merger targets.

Regulators want to see:

Comprehensive assessment of the target’s technology infrastructure, clear plans for addressing identified deficiencies, realistic integration timelines that don’t compromise operational resilience, adequate resources allocated to technology integration, and board-level understanding of technology risks.

Some regulators have delayed transaction approvals until acquiring institutions provided more detailed integration plans.

Preparing Regulatory Filings

Merger applications to banking regulators must address technology and operational risk.

Your filings should demonstrate:

That you’ve conducted thorough bank M&A due diligence, that you understand the technology risks you’re inheriting, that you have concrete plans to address those risks, and that customers won’t experience service disruptions.

Be prepared to supplement initial filings with additional information about technology integration plans if regulators request it.

The Future of IT Due Diligence in Banking M&A

Emerging Technologies Reshaping Due Diligence

Cloud-native architectures, artificial intelligence, blockchain, and open banking APIs are becoming standard components of banking technology stacks.

Due diligence processes must evolve to assess these technologies effectively. Traditional infrastructure assessments don’t fully address cloud security and governance.

Forward-thinking institutions are developing new assessment frameworks specifically for emerging technologies, ensuring their M&A technology audit approaches remain relevant as banking technology continues advancing.

Increasing Regulatory Focus on Technology Risk

Expect regulatory scrutiny of technology risk in M&A to intensify further.

Regulators worldwide are implementing operational resilience requirements that demand robust technology risk management. These requirements will influence how regulators evaluate merger applications and integration plans.

Institutions should anticipate needing to demonstrate increasingly sophisticated technology risk assessment and management capabilities to gain regulatory approval for future mergers.

Conclusion: Making IT Due Diligence Your Competitive Advantage

Comprehensive IT due diligence isn’t just risk management—it’s a competitive advantage in today’s rapidly evolving banking landscape.

Institutions that excel at bank M&A due diligence can identify overlooked acquisition targets, negotiate better deal terms, and execute smoother integrations. Leverage AI tools for M&A IT assessment and create reusable frameworks to build organizational capability.

View IT due diligence as integral to your M&A strategy. Insights from technology audit for bank acquisitions should inform deal structure, pricing, and integration planning.

Banks that master bank mergers IT assessment will turn potential banking IT risks into competitive advantages through effective synergy planning IT M&A.

Key Takeaways

- IT due diligence determines deal success or failure, not just financial valuation.

- Legacy systems, cybersecurity gaps, and regulatory risks are the biggest hidden liabilities in bank acquisitions.

- Core banking compatibility, data architecture, infrastructure, and vendor contracts must be assessed before deal close.

- Limited visibility into target IT environments increases breach, compliance, and cost-overrun risks.

- Integration complexity and operational disruption are primary causes of lost post-merger synergies.

- AI-driven tools improve code analysis, contract review, data quality checks, and threat detection during diligence.

- Accurate IT cost normalization and synergy planning are essential for realistic deal valuation.

- Regulators expect deep technology risk assessment and credible integration plans before approving mergers.

- Secure data migration, governance, and cybersecurity harmonization are critical in post-merger integration.

- Banks that master IT due diligence gain competitive advantage through smoother integration and faster value realization.

Frequently Asked Questions (FAQs)

What are the key IT risks in bank M&A due diligence?

- Legacy core banking incompatibility and technical debt

- Undisclosed security vulnerabilities or breach history

- Non-compliance with FFIEC, OCC, or GLBA regulations

- Vendor lock-ins and costly software contracts

- Data migration failures and operational disruption

Should LLMs be used for M&A research over traditional algorithms?

LLMs should complement—not replace—traditional analytics in M&A research.

- Rapid document summarization and clause extraction

- Pattern detection across contracts, risks, and compliance

- Faster regulatory and technical comparisons

- Limits include hallucinations, auditability gaps, and data privacy risks

How do Big 4 firms handle IT due diligence in bank deals?

- Technology estate and core system assessment

- Cybersecurity and regulatory compliance review

- Vendor contracts, licensing, and third-party risk analysis

- IT cost baseline, normalization, and synergy modeling

- Post-merger integration roadmap and remediation plan

What IT infrastructure checks are essential pre-M&A close?

- Core banking platform health and vendor support status

- Cloud vs. on-premise architecture maturity

- Network resilience, monitoring, and segmentation

- Backup, disaster recovery, and business continuity readiness

- Security operations and incident response capability

Failures here can delay closing or increase integration cost.

How to evaluate target company software contracts in banking M&A?

- License transferability after change of control

- Renewal terms, termination penalties, and lock-ins

- Compliance with banking data and security regulations

- Ongoing maintenance, upgrade, and support costs