Table of Contents

Summarize and analyze this article with

Chat GPT

Perplexity

Grok

Google AI

Claude

Introduction

Why Cloud Migration Becomes Critical in Bank Mergers

When two banks merge, their IT ecosystems rarely align. Core banking platforms, data warehouses, customer identity systems, and compliance controls often operate on different infrastructures. Maintaining parallel legacy systems increases operational cost and slows decision-making. Therefore, cloud migration becomes the fastest path to unified operations, scalable infrastructure, and standardized security.

Cloud platforms also support rapid integration through APIs, automation, and centralized governance. These capabilities help merged banks deliver consistent digital experiences while meeting strict regulatory expectations. Without a clear bank merger cloud migration strategy, institutions risk prolonged integration timelines and declining customer trust.

Key Risks That Derail Banking Cloud Migration

Despite its advantages, cloud migration during bank mergers carries substantial risk. Regulatory compliance remains the most significant barrier. Financial regulators require strict controls around data residency, encryption, and auditability. Any misalignment can lead to penalties or operational restrictions.

Legacy system complexity presents another major challenge. Many banks still rely on monolithic core systems that are difficult to refactor for cloud environments. Migration delays often occur because applications were never designed for distributed architectures.

Cost overruns also threaten merger value. Poor workload assessment, uncontrolled storage growth, and data transfer fees can push migration budgets far beyond projections. At the same time, downtime or transaction failure can directly affect customers and revenue. These risks highlight the need for a carefully governed banking cloud migration strategy supported by experienced execution partners.

Architecture Patterns for Zero-Downtime Migration

Achieving zero downtime cloud migration in banking requires structured architecture decisions rather than simple lift-and-shift approaches. Successful mergers typically rely on parallel run environments where legacy and cloud systems operate simultaneously until validation is complete. This approach protects transaction continuity and enables gradual cutover.

Phased domain migration is another proven model. Instead of moving the entire banking stack at once, institutions migrate specific domains such as payments, lending, or customer analytics in controlled stages. This reduces operational shock and simplifies troubleshooting.

API-led decoupling further accelerates integration. By exposing legacy capabilities through secure APIs, banks can modernize front-end services while core systems transition in the background. Hybrid bridge architectures often support this phase, combining on-premise controls with scalable cloud infrastructure until full migration is safe.

Hybrid vs Multi-Cloud in Post-Merger Banking

Choosing between hybrid and multi-cloud models is a strategic decision during post-merger cloud adoption. Hybrid cloud allows banks to retain sensitive workloads on-premise while moving customer-facing applications to the cloud. This model simplifies compliance and supports gradual modernization.

Multi-cloud strategies, in contrast, reduce vendor lock-in and improve resilience. Banks can distribute workloads across providers such as AWS or GCP to enhance availability and negotiation flexibility. However, multi-cloud governance is complex and requires strong orchestration, security standardization, and cost monitoring. The right choice depends on regulatory exposure, workload sensitivity, and long-term digital transformation goals.

Hybrid vs Multi-Cloud – Quick Comparison

- Hybrid: Strong and easier to manage

- Multi-Cloud: Complex but flexible

- Hybrid: Moderate

- Multi-Cloud: High

- Hybrid: Higher

- Multi-Cloud: Lower

- Hybrid: Lower

- Multi-Cloud: Higher

Cost, Compliance, and Governance Controls

AI-Assisted Cloud Migration in Banking M&A

How PiTech Enables Seamless Banking Cloud Migration

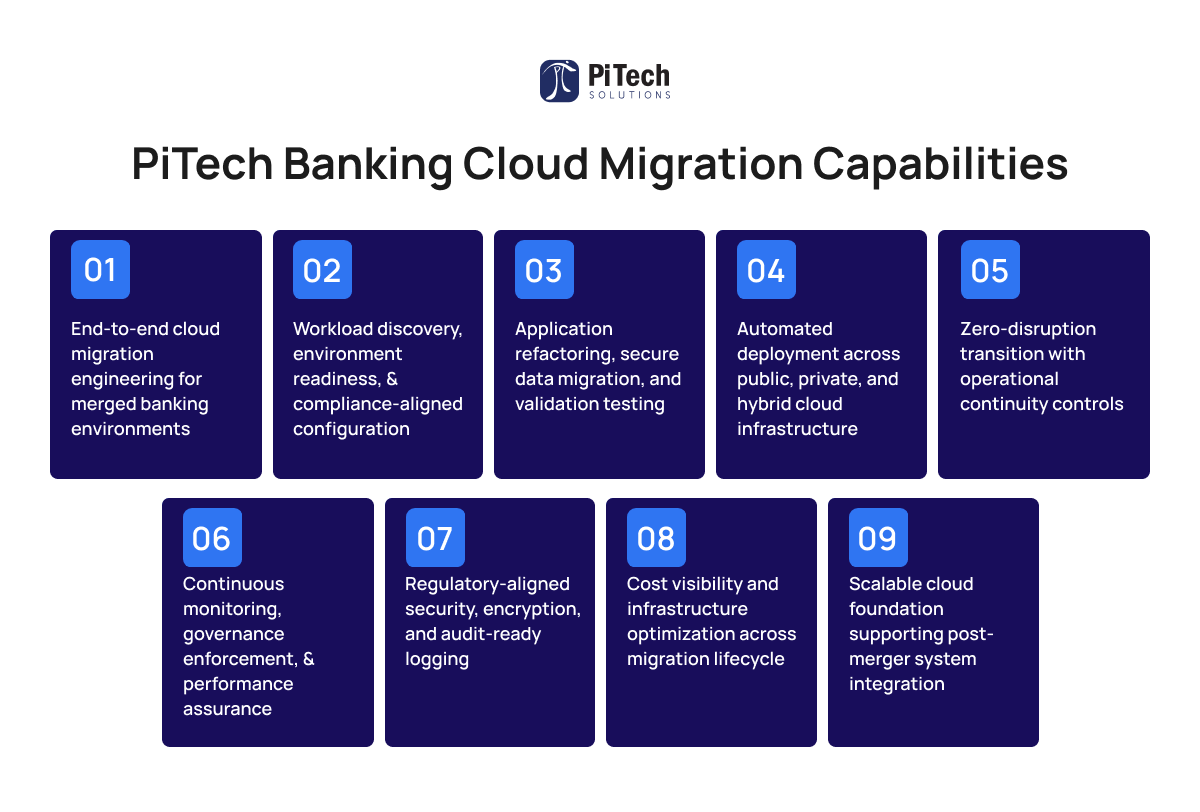

PiTech provides comprehensive, technology-driven cloud migration services for financial institutions undergoing mergers. The delivery model is centered on secure engineering execution, compliance-ready cloud environments, and uninterrupted operational continuity across regulated banking systems.

Execution begins with workload discovery, environment preparation, and compliance-aligned configuration to ensure migration readiness. Automated migration pipelines then manage application refactoring, data transfer, validation testing, and secure deployment across cloud infrastructure. Continuous monitoring, governance enforcement, and performance assurance maintain regulatory alignment, operational stability, and cost control throughout the migration lifecycle.

Through controlled execution, platform reliability, and secure cloud integration, PiTech enables merged banks to transition critical systems efficiently while maintaining service continuity, data integrity, and regulatory compliance on a scalable cloud foundation.

PiTech Banking Cloud Migration Capabilities

Conclusion:

Bank mergers intensify technology risk, operational complexity, and regulatory scrutiny. Cloud migration offers the most effective path to unified infrastructure, scalable services, and long-term efficiency. However, success depends on disciplined governance, zero-downtime architecture, and expert execution. Institutions that adopt structured cloud migration challenges bank mergers strategies can avoid disruption and unlock real merger value. With the right planning and partner support, seamless cloud integration becomes not just possible but transformational for the future of digital banking.

Key Takeaways

- Cloud migration is central to successful bank mergers, enabling unified operations, scalability, and consistent digital experiences.

- Regulation, legacy systems, and downtime risk are the biggest barriers that must be addressed early in planning.

- Zero-downtime execution depends on parallel environments, phased migration, and API-led integration, not simple lift-and-shift.

- Hybrid and multi-cloud strategies must align with compliance, cost governance, and long-term transformation goals.

- AI-assisted discovery, testing, and risk prediction are becoming essential for safe and fast post-merger migration.

- Expert execution and governance ultimately determine merger value realization, making structured migration frameworks critical.

Frequently Asked Questions (FAQs)

How do banks migrate to the cloud during a merger without downtime?

Banks typically use parallel run architectures, phased workload migration, and real-time data synchronization. This allows legacy and cloud systems to operate together until validation is complete, ensuring uninterrupted customer transactions.

What are the biggest cloud migration risks in bank M&A?

The primary risks include regulatory non-compliance, legacy system complexity, cost overruns, downtime, data corruption, and vendor lock-in. These risks increase because merger timelines are compressed and integration scale is large.

What cloud strategy works best for legacy banking systems in mergers?

Most institutions adopt a hybrid-first modernization strategy. Critical or regulated workloads remain on-premise initially, while digital channels and analytics move to the cloud. Gradual refactoring then enables full cloud adoption.

How much does cloud migration cost during a banking merger?

Costs vary by infrastructure scale, refactoring effort, compliance controls, and data transfer. However, poor planning can increase budgets by 20–30%, making FinOps governance and workload optimization essential from the start.

Is multi-cloud better than single-cloud for post-merger banking integration?

Multi-cloud improves resilience and vendor flexibility, but it introduces governance and security complexity. Many banks begin with hybrid or single-cloud and expand to multi-cloud once operational maturity improves.